Every business owner has been there: at the beginning of the month you open up your merchant statement and cringe at all the merchant account fees that were deducted last month. Although these will never completely vanish, you can get a better understanding of where they come from and how to avoid paying more than necessary. In this article, we’ll help you do just that.

What are merchant account fees?

Merchant account fees are the costs for a business owner to accept credit card or debit card payments. It's how your payment provider and the banks that facilitate each transaction get paid for their services.

Think of merchant account fees as the operational cost for running card payments—just like how you pay to lease a space for your office. However, these fees can vary quite a bit depending on your payment provider, credit card types, and the way you accept payments.

What are the different types of merchant account fees?

Merchant account fees come in all shapes and sizes. Depending on the payment provider, it’s more than just the price you pay for each credit card transaction. Here are some of the common fees you’re likely to come across when selecting a payment provider:

1. Transaction fees

Unfortunately, this is a cost you just cannot avoid. It’s the fee you pay every time a customer pays by card—often referred to as “price” on a payment provider's website. Typically, you’ll see either interchange plus, flat rate, or tiered pricing, which although different, are all just transaction fees at their core. These fees will also differ depending on the type of payment—in-person, keyed, or online—with in-person payments being the cheapest and online more expensive due to varying levels of risk.

Top processors with the lowest processing fees for Canadian businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.39% (avg) + $0.25 | 1.76% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% + $0.30 to 3.3% + $0.15 | 2.5% |

| Stripe (flat-rate) | 2.90% + $0.30 + 0.5% for manually entered cards + 0.8% for international cards* + 2% if currency conversion is required | 2.7% + $0.05 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Top processors with the lowest processing fees for U.S. businesses:

| Payment companies | Online fees | In-person fees |

|---|---|---|

| Helcim (interchange-plus) | 2.49% (avg) + $0.25 | 1.93% (avg) + $0.08 |

| Moneris (flat-rate) | 2.85% + $0.30 | 2.65% + $0.10 |

| Square (flat-rate) | From 2.90% to 3.30% + $0.30 | 2.60% + $0.15 |

| Stripe (flat-rate) | From 2.90% + $0.30 + 0.5% for manually entered cards + 1.5% for international cards + 1% if currency conversion is required | 2.70% + $0.50 |

| Clover (flat-rate) | 3.50% + $0.10 | 2.30% + $0.10 |

Curious about how much you could save with Helcim? Submit your merchant statement today and get a personalized savings estimate!

2. Monthly fees

Some providers charge a monthly fee (or occasionally an annual fee) to access your merchant account on top of the basic transaction fees. These can be a flat fee for every merchant, or vary based on the specific services you need. It can vary between $15 and $250, depending on your business and the tools you need.

3. Monthly minimum fee

Some processors will make you pay monthly minimum fees to maintain your account. If your transaction fees don't add up to this minimum, you must pay the difference.

4. User fees

This is an additional fee charged based on the number of users with access to your merchant account. You’ll commonly see it charged on a monthly basis and can be set as a fee per user, or a fixed fee that gives you a maximum number of seats in the account.

5. Deposit fees

This is a fee charged when your funds are deposited in your bank account. Some providers will charge this fee on every deposit or some will offer free deposits, but an additional fee if you wish to have instant deposits instead of waiting a couple days. This fee typically falls between $50 and $200.

6. Setup fees

This is an upfront cost some providers will charge to configure or integrate your account where necessary.

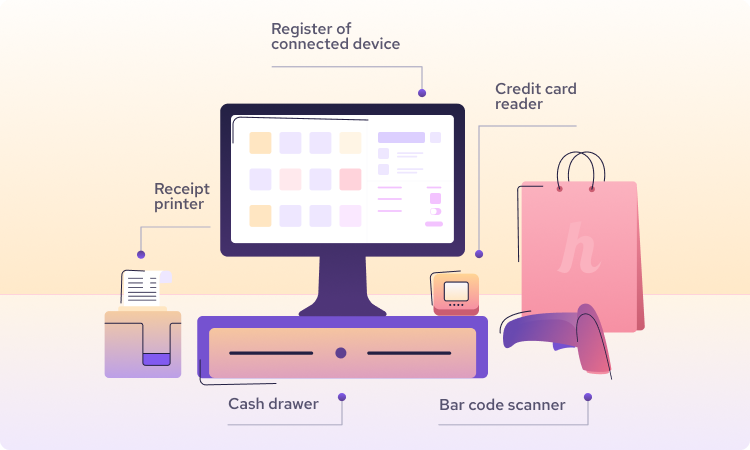

7. Equipment fees

This is the cost to purchase or rent payment hardware for your in-person payments.

- Cash registers can range in price from $100 to over $1,200, depending on their features and capabilities.

- POS screens are typically priced between $200 and $400.

- Tablet stands range from $50 to $400, depending on the design.

- Receipt printers can cost anywhere from $30 to over $600.

- Credit card readers are priced around $100 to $500. The Helcim Smart Terminal, priced at $349 USD, includes a built-in receipt printer, eliminating the need for an additional printer.

- Cash drawers vary between $65 and $650, with higher prices offering more capacity and enhanced security.

- Barcode scanners range from $50 to over $200, with wireless models and advanced scanning features costing more.

You’ll often see different options such as, one time payment, installment plans, or recurring rental payments.

8. Payment gateway fees

A payment gateway fee is charged when using a payment gateway for online transactions. This can be per transaction, monthly, or both.

9. PCI compliance fees

PCI (Payment Card Industry) fees are what you pay the credit card processors to make sure your account is compliant with PCI DSS requirements. Not every provider charges them, but if they do, it’s often a hidden fee to be aware of in your contract. It’s most often charged on a yearly basis, but can also be charged monthly or quarterly.

10. Credit card chargeback fees

A chargeback is when your customer disputes a transaction either due to an issue with their purchased product/service or fraud. Most payment providers will impose chargeback fees to deal with your dispute to cover the time and money it takes them to review. This fee ranges from $20 to $50 per chargeback.

11. Early termination fees (cancellation fees)

If the payment provider enters a contract with you, it often has an early termination fee, meaning you are charged a penalty for leaving the contract before the agreed upon timeline. The early termination fees can range from $250 to over $5,000.

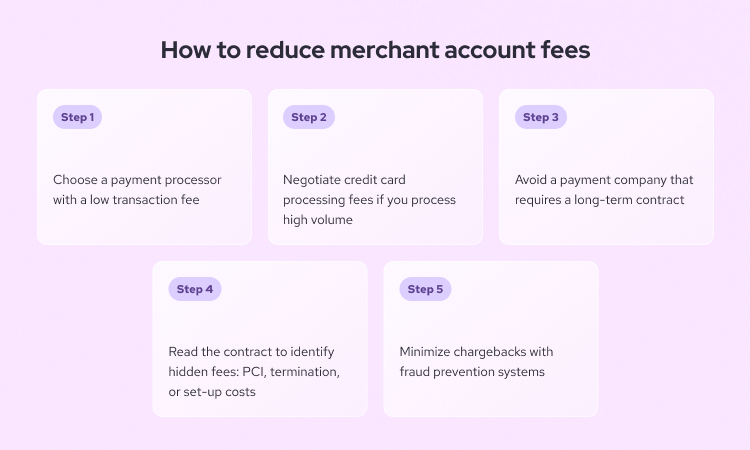

How to reduce merchant account fees

While merchant account fees are part of doing business, you don’t have to settle for sky-high rates. Here’s a few ways you can cut back on fees:

1. Choose an affordable payment processor

Transaction fees are the one fee you are guaranteed to pay. So scan each provider's pricing on their website and find one with lower transaction fees. Often companies, like Helcim, who use interchange plus pricing are the most affordable versus payment processors that charge a flat fee.

2. Negotiate your credit card processing fees

Common practice in the payment industry is to provide lower credit card processing fees to merchants who process higher volumes. If you’re a high volume business, you may be able to negotiate more attractive processing costs with your provider.

3. Avoid contracts

Any payment provider that wants to lock you into a contract likely has a monthly or annual fee, an early termination fee, and/or an equipment rental fee. You’ll most likely find these with the giant payment processors. It is completely avoidable by just picking a more modern payment company who does not offer a contract, and often a better, more affordable product. Learn more about how to escape from contracts in our guide for Canadian and US businesses.

4. Read the fine print

There’s a growing problem in the payment industry with hidden fees. Things like setup, early termination, and PCI compliance fees are all tucked away in the fine print and sneak up on you once you’re already locked into a contract. It is very important to read your contracts carefully so you can avoid paying more than you expected. Or alternatively, just checkout Helcim as we’re fully transparent with our rates—no hidden fees ever.

5. Minimize chargebacks

Chargebacks are not completely avoidable, but can be reduced so you don't have to pay any chargeback fees. One way to minimize chargebacks is to implement fraud prevention systems. You can set up systems to verify credit card payments and ensure they are coming from their rightful owners, preventing a fraudulent transaction, and potential chargeback, before it even happens. Part of this is flagging unusual credit card transactions. Often fraudsters will attempt to buy unusually large quantities of items, or make repeat small quantity purchases. If it seems like atypical behavior from a customer, it could be a fraudster preparing to file a number of chargebacks against you.

Another simple way to avoid an unnecessary chargeback is to make sure your policies and communications are clear. A customer should be able to recognize a charge from you on their credit card statement so they don’t mistakenly file a chargeback thinking it was fraud. If your return policy or support system is convoluted, it may be easier for them to just file a chargeback. So make it simple for them to get a hold of someone and return a product they are not satisfied with.

How Helcim offers the lowest merchant account fees

There are a number of factors that contribute to our low merchant account fees:

1. Interchange Plus pricing

The Interchange plus model is the most affordable option for merchant credit card fees. Instead of charging a flat rate for every transaction, we give you the wholesale cost of the transaction (the interchange rate) and add a small margin on top. So when a customer pays with a cheaper credit card, like a Visa consumer credit card, you pay less. When they pay with a more expensive credit card, like American Express, you pay a bit more. But overall it averages out and you end up paying less than with a flat rate provider, who sets a fixed rate with a much larger margin.

2. No contracts

We don’t lock you into a contract with all the extra monthly fees, rental costs, and early termination charges. Your account is completely free and you can leave and come back anytime you want.

If you're looking to switch to Helcim for lower rates but are currently locked into a contract, Helcim Merchant Buyout Program can cover up to $500 of your cancellation and equipment costs.

3. Full transparency

There are absolutely no hidden fees in our fine print. Everything you pay is listed right on our website for all to see so you don’t have to worry about that surprise charge on your bill at the end of the year.

4. No unnecessary fees

Best of all, we don’t charge the unnecessary extra merchant account fees that the other guys do:

- No PCI compliance fees

- No early termination fees

- No monthly fees

- No setup fees

- No deposit fees

- No user fees

FAQ

Why are my merchant account fees so high?

There could be a number of reasons. (1) You’re on flat rate pricing which is often quite costly to a business. (2) You have a monthly fee or an equipment rental fee that is billing you every month. (3) There are some hidden fees you didn’t notice when you signed the contract.

How do you avoid merchant service fees?

Most of the extra merchant service fees are avoidable just by choosing the right payment provider. When it comes to transaction fees, certain regions and businesses are eligible to pass the fees on to their customers to offset the costs. Features like Helcim Fee Saver make it very easy to do so.

Who pays merchant account fees?

Merchant account fees are typically paid by the business owner as a cost of accepting a credit or debit card, but with services like Helcim’s Fee Saver, you can pass on a portion of these costs to your customers.

What are credit card merchant fees?

Credit card merchant fees are just another way of saying merchant account fees. You might also hear merchant services fees or payment processor fees, but they all essentially are referring to the same type of fees discussed above.

What are interchange fees?

An interchange fee is the fee charged between banks for processing credit or debit card transactions. The fee is set by the card networks (like Visa and Mastercard) and is typically a percentage of the transaction plus a few cents. It varies depending on the type of credit card or debit card used, and whether the transaction was in-person, keyed, or online. This is passed to you as the merchant in your transaction fee.