-

Content

Last Updated on September 17, 2024 by Robert Luong

Interchange plus pricing is the most transparent and cost-effective pricing model for credit card processing.

According to MPC in 2024, U.S. businesses paid $100 billion in credit card processing fees to Visa and Mastercard, highlighting just how important it is for merchants to reduce these costs.

In this guide, we’ll walk you through how interchange plus pricing works, how to calculate it, and why it could be the perfect fit for your business.

What is interchange plus pricing?

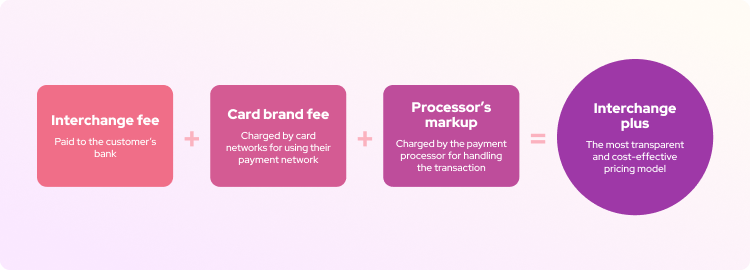

To understand interchange plus pricing, it’s important to know the three main components of credit card processing fees: the interchange fee, card brand fee, and the processor's markup.

-

Interchange fee is paid to the customer’s bank, covering the risk and cost of processing the transaction. This fee fluctuates with each transaction based on factors like the card type (privilege, travel rewards cards, etc.), how the transaction is processed (in-person or online), and your industry.

-

Card brand fees, also known as assessment fees, are charged by card networks (like Visa, MasterCard, and American Express) for using their payment network. They cover the cost of using the card network infrastructure.

-

The processor's markup is the fixed markup added by the payment processor on top of the interchange fee.

Since the interchange fee varies, your credit card processing fees will fluctuate as well. To simplify things, many processors charge a flat rate for every transaction, such as 2.90% + $0.30.

On the other hand, processors like Helcim use interchange plus pricing that passes the actual cost of each transaction, plus a transparent margin. For example, interchange + card brand fee + 0.40% + 8¢. This pricing model often saves merchants around 25% on fees compared to the flat rate pricing model.

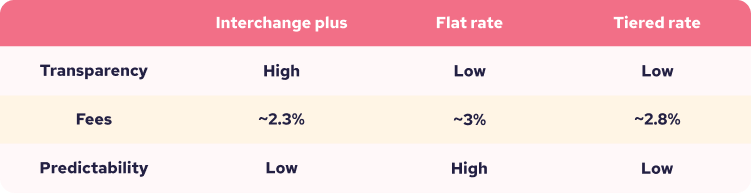

Interchange plus vs flat rate vs tiered pricing models

Now that you understand the three components of processing fees and how interchange plus works, let’s compare it with two other common pricing models: flat rate and tiered pricing.

Interchange plus pricing breaks down the credit card processing fees into the interchange fee, card brand fee, and processor's markup. This pricing model is highly transparent and allows businesses to see exactly what they’re paying for each transaction, making it one of the most cost-effective options compared to other pricing models.

Flat rate pricing charges a single fixed fee for all transactions, regardless of the actual cost to process them. While simple, these flat rates are set high enough to guarantee profitability, meaning you often overpay for it. Besides, you have no idea how much you're paying on top of what the payment processor pays for the transaction.

Tiered pricing groups transactions into qualified, mid-qualified, and non-qualified tiers, with each tier having different fees based on the card type and how the transaction is processed. Qualified transactions get the lowest fees, while non-qualified ones have higher fees. The main issue with tiered pricing is its lack of transparency as processors often don't clearly explain how transactions are categorized. As a result, tiered pricing may be more expensive and harder to predict than interchange plus or flat rate pricing models.

What are the pros and cons of interchange plus pricing?

Interchange plus pricing is the most transparent and cost-effective pricing model available, but it still comes with its own drawbacks. Understanding the pros and cons can help you decide if it’s the right fit for your business.

1. Pros of interchange plus pricing

Transparency: With interchange plus pricing, your monthly merchant statement typically breaks down all the fees, showing exactly what they’re for. This allows you to see which cards and transaction types are more or less expensive. Because these statements itemize every fee, it helps eliminate hidden charges that some processors might try to slip into merchant statements.

Not overpaying: Since transaction costs fluctuate, some transactions will have lower fees than others. With the flat rate pricing model, every transaction is charged the same fee, regardless of its actual cost. In contrast, interchange plus pricing passes on the true cost of each transaction, ensuring you’re not overpaying. This makes it significantly more cost-effective than flat rate pricing models.

Scalability: Payment processors offering interchange plus pricing may include volume discounts once you surpass a certain transaction threshold each month, allowing you to save more as you process more. For example, Helcim automatically reduces your payment processing fees as your transaction volume increases.

Benefit from lower fees as interchange rates are updated: Card brands frequently adjust their interchange rates yearly. With an interchange plus, your business automatically benefits whenever these rates are lowered. When the interchange rate changes, the new rate will be reflected in your statement. In contrast, with a flat rate pricing model, your payment processing fee stays the same even if your processor is being charged less due to a lower interchange rate.

2. Cons of interchange plus pricing

Fluctuations: Since interchange fees change based on factors like the type of card used (credit, debit, or rewards) and the transaction method (in-person, online, or manually entered), your payment processing fees will fluctuate with each transaction. This can make it harder to accurately forecast your monthly processing costs.

Complexity: The breakdown of fees into interchange, card brand fees, and the processor's markup can be more difficult to understand. As a result, businesses need to carefully review their statements to understand what they’re being charged.

How much can you save with interchange plus pricing?

Interchange plus pricing can be harder to predict since the fee for each transaction fluctuates. However, it remains the most cost-effective pricing structure for businesses. Below are the average savings each industry has with Helcim’s interchange plus compared to flat rate credit card processors in 2025.

| Industry Market | Total Savings (%) |

|---|---|

| Automotive | 28.31% |

| Cab & Delivery | 27.14% |

| Charity & Non-Profit | 31.04% |

| Contractors & Home Services | 26.37% |

| Education | 33.09% |

| Enterprise & Utilities | 48.45% |

| Financial Institution | 24.40% |

| Gas Stations | 40.54% |

| Government | 41.54% |

| Health, Beauty & Wellness | 31.62% |

| Healthcare | 25.09% |

| Hotels & Lodging | 23.36% |

| Online Sales | 20.66% |

| Organizations & Associations | 27.06% |

| Platforms, Apps & SaaS | 20.20% |

| Professional Services | 27.68% |

| Recreation | 27.01% |

| Restaurant | 31.49% |

| Retail Goods | 25.00% |

| Transportation | 20.36% |

| Wholesale | 23.23% |

If you’re curious about how much you could save with interchange plus pricing, submit your statement here, and our team will provide you with a personalized savings estimate.

How do you calculate interchange plus rate?

To calculate the interchange plus rate, you need two key components: the interchange fee for each card brand and the processor's markup.

1. Use the Helcim pricing calculator

You can use the Helcim pricing calculator to calculate the interchange plus rate. The tool breaks down the credit card processing costs by the interchange fee, card brand fee, and Helcim’s markup.

2. Calculate interchange plus rate manually

If you prefer to calculate the rate manually, simply use the formula: interchange plus rate = interchange fee + card brand fee + processor's markup.

For example, let’s say a customer buys a donut at your shop in Texas using a Visa Credit CPS card. The transaction is in-person (card-present) so the fees are the following:

- Interchange fee: 1.29% + 10¢

- Card brand fee: 0.24% + 2¢

- Helcim’s markup: 0.40% + 8¢

As a result, the total credit card fee for this transaction would be the sum of the three fees, totaling 1.93% + 20¢. This fee is much lower than the flat rate that other credit card processors charge, such as:

- Square: 2.60%

- Stripe: 2.90% + 0.30¢

- Clover: 2.30% + 0.10¢

Are debit and credit interchange plus rates different?

Interchange plus pricing applies to both credit and debit card transactions, using the same formula: the sum of the interchange fees, card brand fees, and payment processors' margin.

However, debit card transactions typically have lower interchange fees than credit cards because they carry less risk for the customer’s bank. With debit cards, funds are directly withdrawn from the customer’s account, meaning they can only spend what they have. In contrast, credit card transactions involve higher fees since the bank is essentially lending money to the customer, carrying the risk of default if the customer is unable to repay.

Good interchange plus rate for credit transactions

A good interchange plus rate depends on where the credit card transaction is processed and the card brand used.

- In-person (card-present) transactions typically have lower interchange fees than online (card-not-present) transactions due to the lower risk of fraud and chargeback.

- Different card brands—like Visa, Mastercard, or American Express—have varying interchange and card brand fees, with premium or rewards cards often carrying higher fees.

1. Good rates for in-person transactions

In the United States, Visa currently offers some of the lowest interchange and card brand rates. For more details and comparisons, please visit the Helcim pricing calculator.

| Card type | Interchange rate | Card brand fee |

|---|---|---|

| Credit CPS | 1.29% + 10¢ | 0.24% + 2¢ |

| Credit Rewards Traditional | 1.43% + 10¢ | 0.24% + 2¢ |

| Credit Rewards Signature | 1.43% + 10¢ | 0.24% + 2¢ |

| Credit Rewards Signature Preferred / Infinite | 1.88% + 10¢ | 0.24% + 2¢ |

| Credit Corporate Level 2 | 2.10% + 10¢ | 0.24% + 2¢ |

In Canada, Mastercard currently offers some of the lowest interchange and card brand rates.

| Card type | Interchange Rate | Card brand fee |

|---|---|---|

| Consumer (Core) | 0.92% | 0.10% + 1¢ |

| Premium (World) | 1.22% | 0.10% + 1¢ |

| High-Spend (World Elite) | 1.56% | 0.10% + 1¢ |

| Super Premium (Muse) | 1.65% | 0.10% + 1¢ |

| Corporate | 2.00% | 0.10% + 1¢ |

2. Good rates for online transactions

In the United States, Discover currently offers the lowest interchange and card brand rates for online debit card transactions.

| Card type | Interchange Rate | Card brand fee |

|---|---|---|

| Credit Core | 1.89% + 0.1¢ | 0.13% + 2¢ |

| Credit Rewards | 2.00% + 0.1¢ | 0.13% + 2¢ |

| Credit Premium | 2.00% + 0.1¢ | 0.13% + 2¢ |

| Credit Premium Plus | 2.40% + 0.1¢ | 0.13% + 2¢ |

| Credit Corporate Level 2 | 2.30% + 0.1¢ | 0.13% + 2¢ |

In Canada, Visa currently offers some of the lowest interchange and card brand rates.

| Card type | Interchange Rate | Card brand fee |

|---|---|---|

| Consumer | 1.40% | 0.10% |

| Infinite | 1.65% | 0.10% |

| Privilege | 2.40% | 0.10% |

| Corporate | 2.00% | 0.10% |

Good interchange plus rate for debit transactions

Similar to credit card transactions, the interchange plus rate for debit cards also depends on where the transaction is processed and the card brand being used.

1. Good rates for in-person transactions

In the United States, Mastercard currently offers some of the lowest interchange and card brand rates.

| Card type | Interchange Rate | Card brand fee |

|---|---|---|

| Debit Regulated | 0.05% + 22¢ | 0.13% + 2¢ |

| Debit Business Regulated | 0.05% + 22¢ | 0.13% + 2¢ |

| Debit | 1.05% + 15¢ | 0.13% + 2¢ |

| Debit Business | 1.65% + 10¢ | 0.13% + 2¢ |

In Canada, Mastercard and Visa currently offer the same interchange rates:

- Debit Retail: 0.250% + 5¢

- Debit Grocery: 0.150% + 5¢

- Debit Gas Station: 0.150% + 5¢

2. Good rates for online transactions

In the United States, Discover currently offers some of the lowest interchange and card brand rates.

| Card type | Interchange rate | Card brand fee |

|---|---|---|

| Debit | 0.00% | 0.13% + 2¢ |

| Debit Regulated | 0.05% + 0.22¢ | 0.13% + 2¢ |

In Canada, Mastercard and Visa currently offer the same interchange rates for online debit card transactions:

- Debit Keyed: 1.150%

- Debit Utilities: 0.000% + 10¢

Save 25% on fees with Helcim interchange plus

If your business wants to accept credit cards at a low cost without monthly fees, contracts, or hidden charges, Helcim is the ideal solution. Why should you process credit cards with Helcim?

- Helcim offers 25% lower fees on average compared to other flat-rate credit card processing companies like Square, PayPal, or Stripe.

- You get a free merchant account and tools for accepting in-person and online payments, such as online invoice system, virtual terminal, and POS software.

- You only pay transaction fees. There are no hidden fees, no monthly fees, and no long-term contracts that lock you in.

Sign up now and start accepting credit cards at a low cost with Helcim.

If you're ready to switch to Helcim but feel stuck with your current provider, we’ve got you covered. Our Merchant Buyout Program offers up to $500 in credits to cover your contract cancellation or equipment costs.

Besides, we'll guide you through the entire process—from handling cancellation paperwork to migrating your data to Helcim.

Break up with your current provider for better service and lower fees. Switch to Helcim with our Merchant Buyout Program.

Break up with bad rates.

Feeling stuck with your provider? We'll waive $500 of your processing fees when you switch to Helcim.

FAQ

How does interchange plus pricing work?

The interchange plus pricing model breaks down credit card processing fees into three components: the interchange fee (paid to the customer’s bank), the card brand fee (paid to Visa, Mastercard, etc.), and the payment processor's margin. Unlike the flat rate pricing model, interchange plus passes the true cost of the transaction to your business. For example, a typical fee might be interchange + card brand fee + 0.40% + 8¢.

What is the interchange fee limit?

The interchange fee limit refers to the cap set by some countries on the amount card networks can charge for processing debit or credit card transactions. For example, in the European Union, interchange fees are capped at 0.2% for debit cards and 0.3% for credit cards. In the U.S., there’s no cap for credit card interchange fees, but for debit cards, the Durbin Amendment limits fees to 0.05% + 22¢ per transaction for regulated banks.

What is the interchange rate?

The interchange rate is the fee set by card networks like Visa, and it’s paid to the customer's bank. This fee compensates the bank for handling and processing the transaction. The interchange rate varies based on factors such as the type of card used (credit, debit, rewards), the transaction method (in-person, online), and the business's industry.

How do I avoid interchange fees?

With Helcim Fee Saver, you can avoid paying interchange rates and payment processing fees by passing these costs directly to your customers, allowing you to retain 100% of your sales revenue.

Who makes money on interchange fees?

Issuing banks, the banks that issue credit or debit cards to customers, make money on interchange fees. When a customer swipes their card, the issuing bank collects the interchange fee as compensation for managing the transaction, extending credit, and handling things like fraud protection.

Are interchange fees negotiable?

No, interchange fees are not negotiable. They are set by card networks like Visa and Mastercard and apply to all merchants. Interchange plus pricing is the most transparent and cost-effective pricing model for credit card processing.

According to MPC in 2024, U.S. businesses paid $100 billion in credit card processing fees to Visa and Mastercard, highlighting just how important it is for merchants to reduce these costs.

In this guide, we’ll walk you through how interchange plus pricing works, how to calculate it, and why it could be the perfect fit for your business.

The ultimate guide to accepting credit cards.

Discover essential knowledge and industry insights to increase your bottom line.

Related Articles

-

How to use the Helcim Rate Calculator

Ryleigh Stangness | May 19, 2023

-

US Merchant Guide: New October Interchange Rates 2022

Ryleigh Stangness | December 16, 2022

-

Flat Rate Pricing: What You Need to Know

Danny Randell | November 17, 2022

-

Interchange Plus vs Flat Rate Pricing: Which one is more affordable?

Danny Randell | September 13, 2022

-

Interchange fees ultimate guide A-Z

Miranda Russell | April 3, 2022

-

The Ultimate Path to Choosing a Payments Provider

Jeff Merkel | December 11, 2020

-

Understanding Different Payment Processing Pricing

Chris Reid | September 12, 2020