-

Content

For new businesses, setting up merchant services is one of the most important steps in being able to accept payments beyond cash. For established businesses, maybe your past experiences with merchant services haven’t been great, and now you’re back on the hunt for a better provider.

No matter where you are on your business journey, you don’t have to figure it out alone. This guide will walk you through everything you need to know about merchant services: what they are, why they matter, and how to choose a provider that actually supports your business. By the end, you’ll feel confident about finding a partner that helps you get paid quickly, securely, and without hidden costs.

What are merchant services?

Merchant services give businesses the tools and services they need to accept customer payments. This can mean providing payment terminals, POS systems, or online processing solutions. It also means handling transactions in the background and depositing funds into your business bank account once a payment is settled.

Merchant services also go further than just moving money. They help merchants resolve credit card chargebacks, stay compliant with PCI standards, and manage other payment-related issues. The goal is clear: help businesses accept payments smoothly and securely.

What is the difference between merchant services and merchant accounts?

You use a merchant account to access merchant services. Think of it like your login to online banking; your merchant account is the credential that lets you log in to the merchant service dashboard and use the payment tools.

A merchant account also stores key details about your business: tax settings, company info, product or service details, customer data, payment history, etc. It acts as your business identity in the payments system, making it possible for providers to move money from your customers’ banks to your business bank account.

What are the benefits of using merchant services?

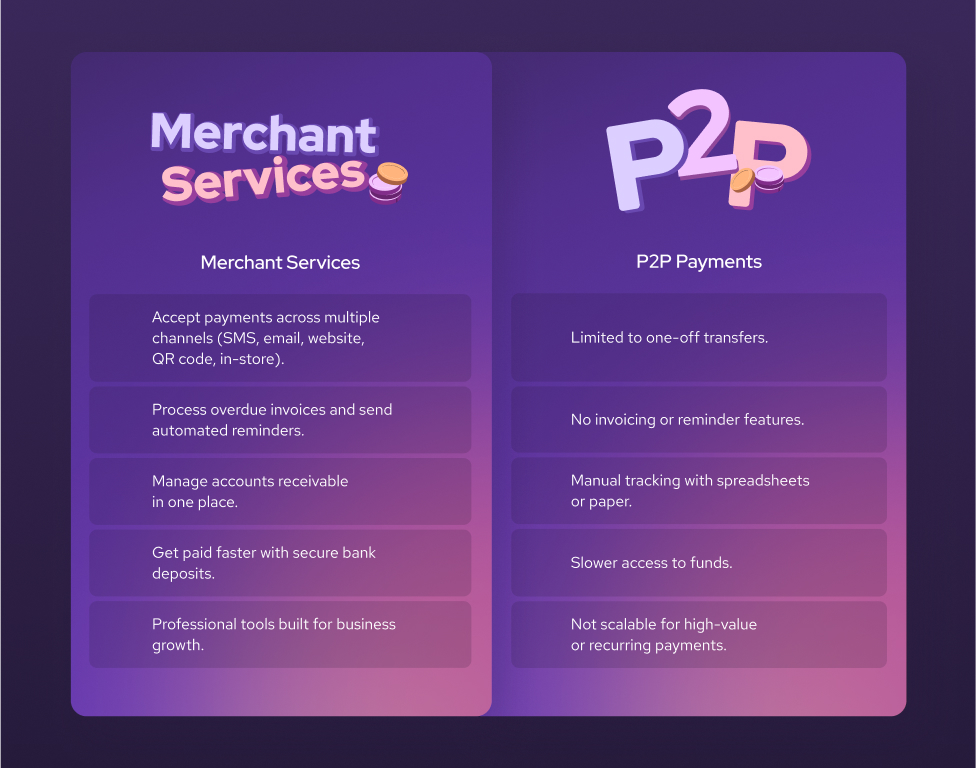

If you still rely on manual P2P payments like bank transfer or cash, then your business will have a hard time to grow and accept more customers. This is because you’re limited to the number of sales channels and payment methods that you can accept. That’s where merchant services come in. It provides your business with a streamlined and structured system to accept payment from your customers in person and online.

Below are the main benefits of using merchant services for your business:

- More sales and more customers

- Faster cash flow and access to funds

- Better customer experience and convenience

- Boost transaction size and customer loyalty

- Easier record-keeping and reconciliation

1. More sales and more customers

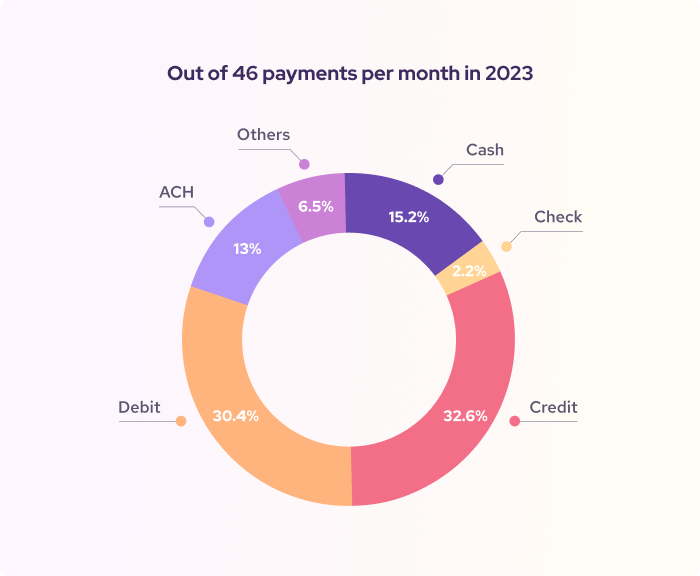

Merchant services give you the tools to accept cards and digital payments, which boosts your sales and attracts more customers. Credit cards alone account for 32.6% of consumers’ monthly payments, and even cash-preferred shoppers use credit cards for about 15% of their purchases. On average, businesses see a 17% increase in revenue after accepting digital payments.

Learn more: Should cash only businesses accept credit cards?

2. Faster cash flow and access to funds

Merchant services let you collect payments across multiple channels—SMS payments, email, website, QR code payments, in-store, and more. You can also process overdue invoices, send reminders for late payments, and collect your accounts receivable in one place. As a result, you get paid faster and can reinvest in your business sooner. Without merchant services, you’d be stuck managing customer payments manually through spreadsheets or paper, and cash-only payments simply aren’t realistic for high-value services.

3. Better customer experience and convenience

When was the last time you saw a customer bring $10,000 in cash to pay for services or hand you a check to deposit at the bank? It’s inconvenient, unsafe, and outdated. With merchant services, you can process large payments quickly through secure digital networks, whether your customers are across town or across the country.

You can also offer multiple payment options: credit cards, debit cards, contactless payments, mobile wallets, ACH transfers, or EFT in Canada. Your customers will appreciate how quick, safe, and hassle-free it is to do business with you, whether they’re tapping a card at your terminal, checking out on your website, or transferring funds online.

4. Boost transaction size and customer loyalty

Visa’s research shows that the average credit card transaction is nearly double the size of the average cash transaction. If your business only accepts cash, customers are limited to the money in their wallets. Accepting credit cards removes that limit, making it easier for customers to buy more.

Merchant services also give you tools to encourage repeat business. You can create discount codes for loyal customers, run holiday promotions, and use built-in CRM tools to handle refunds, returns, chargebacks, and fraud quickly. This builds trust and shows customers that doing business with you is safe and reliable.

5. Easier record-keeping and reconciliation

With merchant services, every transaction is recorded automatically, and your inventory updates across all sales channels. This is especially important if you operate multiple store locations or sell both online and in person, as it gives you a real-time view of sales, inventory, and finances.

You can also download and read detailed processing statements from your provider to review monthly sales, fees, refunds, and profits. This makes it easier to reconcile your books. Some providers, like Helcim, even integrate directly with accounting platforms such as Xero and QuickBooks, so your sales and fees sync automatically.

Who needs merchant services?

Any business that wants to accept digital payments beyond cash or checks will need merchant services. If you plan to take credit or debit card payments—whether in person, online, or by phone—you need merchant services.

Here are some types of businesses and organizations that typically need merchant services:

Retail stores and restaurants: Brick-and-mortar shops, boutiques, cafes, and restaurants use merchant services to set up POS systems, card readers, or payment terminals so they can accept in-person card payments.

E-commerce and online businesses: Online merchants need merchant services to power their website and online stores’ checkout pages (hosted payment pages), where customers can pay for items they add to their carts.

Service providers and professionals: Consultants, freelancers, salons, contractors, and medical or dental offices use merchant services to send invoices, collect in-person payments with credit card machines, set up retainer payments, collect overdue payments, and manage their accounts receivable.

Non-profit organizations: Charities and non-profits benefit from merchant services because donors can contribute via credit or debit card, both online and in person. Merchant services help process donations securely and deposit them safely into the organization’s bank account.

Businesses with recurring billing or subscriptions: SaaS companies, gyms, and other membership-based businesses use merchant services to charge customers on a set schedule. More complex SaaS platforms can use payment integration, such as Helcim API or HelcimPay.js, to customize payment flows that match their pricing models. These solutions also ensure customer payment information is stored securely and processed automatically.

What is included in merchant services?

When you sign up with a merchant service provider, you gain access to a suite of tools that let you accept payments online and in person, along with other services that help you serve customers more effectively. Below is everything typically included in merchant services:

1. Payment processing

When customers pay with debit cards, credit cards, or ACH/EFT transfers, the merchant service provider receives the transaction details from your POS hardware and equipment, or payment tools. It then communicates with the payment networks and the customer’s bank to move funds into your business bank account.

2. Surcharging feature

Each time a provider processes a transaction, it charges a payment processing fee. For credit cards, this fee usually ranges from 2% to 3.5%, depending on the provider. If you want to pass credit card fees to your customers, some providers like Helcim offer a free credit card processing feature (Helcim Fee Saver). When customers choose to pay by credit card instead of lower-cost options like debit, the processing fee is added to their final bill.

3. Point-of-sale (POS) systems

Your provider can equip you with both POS hardware (it’s not free) and software to accept payments. POS hardware can include card readers, payment terminals, kiosks, or traditional registers. These devices work with POS software to process card-present transactions and update your sales and inventory in real time. If you don’t want to invest in hardware, you can use Helcim Tap to Pay on iPhone to collect payments right from your iPhone.

4. Payment page for websites

For e-commerce or any business that needs an online checkout page, a payment page is the right tool. It’s a secure checkout page you can embed on your website or link customers to directly. Providers like Helcim offer pre-built payment pages you can launch quickly, or you can use Helcim API or HelcimPay.js if you want to build a customized checkout flow.

5. Virtual terminal

If you often take payments by phone or mail (MOTO transactions), a virtual terminal is essential. You can enter card details provided by your customer to process the payment on their behalf, retrieve stored payment information for repeat charges, and collect overdue invoices or account balances more efficiently.

6. Invoicing tool

For service-based businesses, invoicing is a key part of getting paid. Providers include invoicing tools that let you send one-time or recurring invoices by SMS or email. These aren’t static PDFs—customers can click a “Pay” button in the invoice to complete their payment immediately. You can also customize the invoice branding and set up automated reminders to reduce overdue invoices.

7. Recurring payments

If your business relies on subscriptions billing or retainers, recurring payment software is a valuable tool. You can create billing schedules that fit your needs, monthly, yearly, or anything in between. You can also add one-time setup fees for onboarding. Providers like Helcim even offer payment recovery features that automatically retry failed transactions, keeping your cash flow steady without interruption.

8. Level 2 and Level 3 credit card optimization feature

Every time a customer pays by credit card, the payment details go straight to the card networks for processing. Networks like Visa and Mastercard reward merchants with lower processing fees if the transaction includes extra data—such as tax amount, customer code, business tax ID, product SKUs, quantity, and unit of measure.

Helcim makes this easy with Level 2 and Level 3 credit card processing. When customers use eligible business, corporate, or purchasing cards, Helcim automatically adds the required Level 2/3 data so your transactions qualify for reduced fees.

Because card networks have strict rules, you won’t see the reduced fees on every transaction right away. Instead, the savings appear as a retroactive adjustment, usually within 45 days, so you’ll notice the credits on the following month’s statement.

9. Reporting and analytics tools

Most providers give you access to dashboards or reports to track your sales, transactions, stock level, most profitable products, and so much other data to manage your business. You can also use the reporting tool to access a complete history of customer interactions, past invoices, and outstanding orders to deliver a personalized service. Learn more about how to use payment data to optimize your business.

10. Customer portal

If you’re a Helcim merchant, your service also comes with a Customer Portal—a secure online hub that puts your customers in control. Through the portal, they can log in anytime to update their information, review their history with your business, and pay outstanding invoices on their own.

You can brand the portal to match your business. Update fonts, logos, and colors so the experience feels seamless and consistent wherever customers interact with you. Best of all, you don’t need to set up a website or manage servers. Just share your branded portal link and customers can log in, or even create an account. You decide what they see and how they access it, all without any coding.

11. Fraud prevention tool

While not a “product” per se, merchant services also give you access to your provider’s support team for any payment-related issues. For example, Helcim Fraud Defender helps you detect risky or suspicious transactions. This lets you double-check customer information, review order details, and call to confirm with the customer before shipping products. The tool protects your business from fraud and helps minimize losses.

What are the costs associated with merchant services?

Merchant services give you all the tools and systems to process payments and manage your business, but “what is this going to cost me?”. Below are the main costs that you can expect from using the merchant services:

1. Credit card processing fees

For every credit card transaction, your merchant service provider charges a percentage of the sale as a payment processing fee. This fee actually has multiple parts:

- The interchange fee is paid to the cardholder’s bank

- The assessment fee is paid to the card network such as Visa, Mastercard, Discover, and American Express

- The markup or service fee that goes to your merchant service provider

While lots of providers charge a fixed expensive fee from 2.5% to 3.5%, Helcim uses the interchange-plus pricing model that offers a “wholesale”, low credit card processing fee to you. Helcim merchants often save 25% on credit card processing fees with Helcim.

Want to see how much you can save with Helcim? Download the completed fees comparison cheat sheet below.

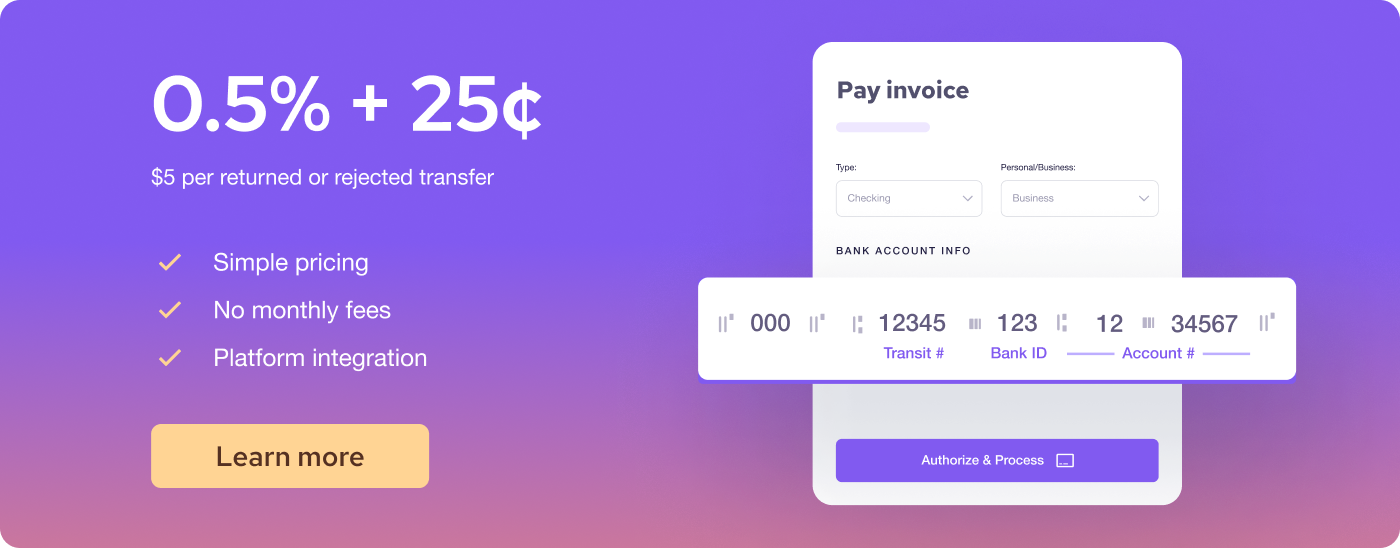

2. ACH processing fees

If your business is in B2B industries, often offers high-value services/items, collects recurring invoices, or relies on automatic payments, ACH payments (for the U.S.) or EFT payments (for Canada) are the common payment methods. The good news is that ACH processing fees are much lower than credit card processing fees. For example, Helcim charges 0.5% + 25¢ per transaction. Also, the ACH transaction fee is capped at $6 for transactions below $25,000, so that you can keep more money to reinvest.

3. POS and payment hardware costs

To accept in-person payments, you’ll need equipment like card readers, payment terminals, or full POS systems. Hardware alone can cost anywhere from $600 to $4,000. If you choose a traditional server-based POS setup, you may also need to host your server, which can run $2,000–$5,000 to buy outright or $70–$300+ per month to rent. On top of that, installation fees for these systems can add another $500.

With a cloud-based POS, hardware costs are similar, but you avoid server expenses since storage and security are handled by your provider’s servers.

4. Monthly fees

Many merchant service providers charge monthly fees to use their software. These fees often exist because the software is specialized for certain industries. For example, Toast’s POS is built specifically for restaurants, offering features like menu management and kitchen order tracking. That added functionality comes with the monthly cost.

If your business doesn’t need a sophisticated system, you can choose Helcim, which includes all payment tools with no monthly fees. This way, you can start accepting payments and grow your business without unnecessary overhead.

On top of monthly software fees, some providers also charge monthly hardware fees if you lease your payment terminals or POS devices instead of buying them outright.

5. Credit card chargebacks and ACH/EFT return fees

Not all transactions you process are legitimate. Sometimes you may accidentally accept a fraudulent payment. Fraudsters can use stolen payment information to buy your products or services, and when the real cardholder notices the unauthorized charge, they issue a chargeback. Each chargeback comes with a fee of $15 to $20. If you’re a Helcim merchant, this fee is refunded when you successfully dispute the chargeback.

The same risk applies to ACH/EFT transfers. If you process a bank transfer that the customer didn’t authorize, the ACH/EFT payments will be returned and your provider will charge a return fee of $10 to $15. Unlike chargeback fees, these return fees are non-refundable.

6. Other unnecessary fees

Aside from the credit card and ACH payment processing fees, you may pay some fixed, unnecessary costs for certain services, such as:

- PCI compliance fees: PCI DSS (Payment Card Industry Data Security Standard) is mandatory for any business that accepts card payments. Some providers, like Helcim, help you stay compliant free of charge, but others charge hundreds or thousands of dollars per year to keep you compliant. Some providers also charge fees if you’re not compliant too.

- Contract termination fees: If you’re locked into a long-term merchant services contract, you may be charged an early termination fee if you cancel before the term ends. These fees vary, but they can range from a few hundred dollars to the full amount of the remaining contract value.

- Administrative fees: Some providers add catch-all “admin” charges for handling account maintenance, customer support, or other back-office functions.

- Application fees: A few providers still charge upfront application or setup fees when you first apply for a merchant account.

- Statement fees: Providers may charge a monthly fee for generating and mailing paper statements. Even with electronic statements, some still tack on a “statement fee” for reporting.

- Setup fees: These are one-time charges for setting up your account, configuring POS systems, or installing hardware. Some providers waive them, while others use them as a standard onboarding cost.

- Monthly minimum fees: If your contract requires a minimum processing volume but you fall short, your provider may charge you the difference. For example, if you agree to $5000 in fees but your provider only collects $4500, you’ll pay the extra $500 to cover the gap.

How do merchant services work?

Let’s say you sign up for a merchant service and open a merchant account. You’ll then get access to a suite of tools to accept payments, such as invoicing software, a virtual terminal, or a POS system. Once you’ve chosen your tools, you can start accepting payments from customers. From there, one of the key roles of merchant services begins: moving money from your customers’ bank accounts to your business bank account.

Depending on the payment method, credit card, debit card, or ACH/EFT, the process works a little differently. Below is how money moves across the credit card and ACH/EFT networks thanks to the merchant services.

1. How merchant service providers process credit card payments

Step 1 – Authorization: The process starts when a customer pays with a credit card—by tapping, inserting, or swiping at your terminal, or by entering card details at an online checkout. The terminal sends the transaction details (credit card number, cardholder name, purchase amount) to your merchant service provider, which then routes the request through the card network.

Step 2 – Authentication: The card network identifies the issuing bank (for example, Citi) and forwards the request. The bank checks whether the card is valid, screens for fraud, and confirms the cardholder has enough available credit. If everything is clear, the bank sends back an approval code through the network to your merchant service provider. The provider relays this message to your terminal or gateway, showing that the transaction is approved and the purchase can go through.

Step 3 – Settlement: At the end of the business day, the card network moves the approved funds from the cardholder’s bank to your merchant service provider, which then deposits them into your business bank account. Learn more about payment processing time.

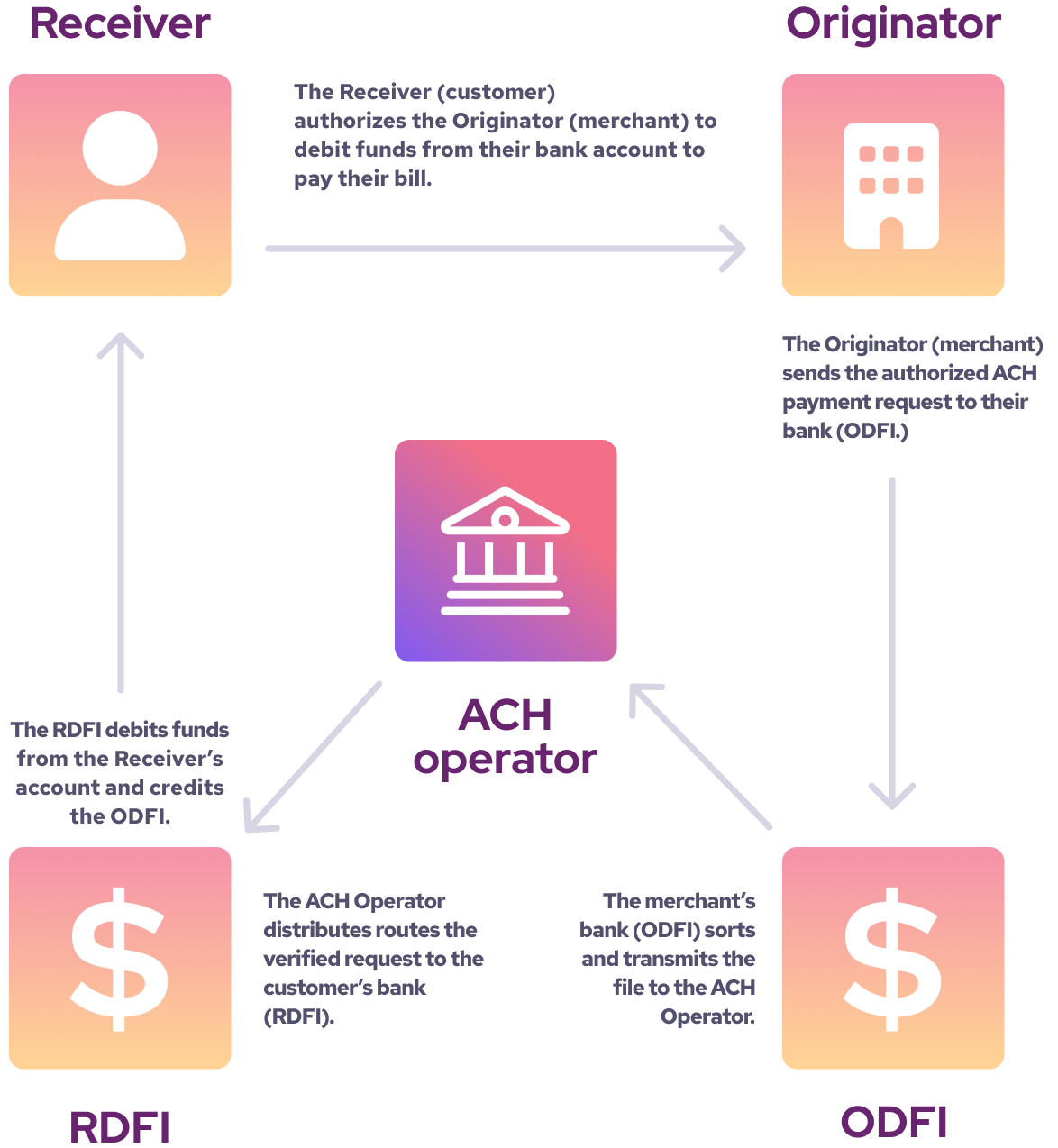

2. How merchant service providers process ACH/EFT payments

Step 1 - Initiation: You start by creating an ACH authorization form and collecting your customer’s signature. This form lists their account and routing numbers and gives you permission to withdraw money from their checking account, either as a one-time payment or on a recurring schedule.

Step 2 - Submission to the ACH network: When it’s time to collect, a merchant service sends an ACH debit request with the customer’s banking details and the payment amount. The ACH network acts as the middleman, checking the request for accuracy and routing it between the customer’s bank and your bank.

Step 3 - Batch processing: To save time and cost, the network doesn’t process each transaction separately. Instead, it groups all ACH requests from that day and settles them together in a batch, typically at day’s end.

Step 4 - Clearing and settlement: The ACH network verifies that the account details are valid and that the customer has enough funds. If everything checks out, money is transferred from the customer’s bank to your bank. If not, the payment is returned, this is known as an ACH return. This usually happens when funds aren’t available, account details are wrong, or the customer disputes the charge.

Step 5 - Completion: Finally, your merchant service provider receives the funds and deposits them into your business account. Depending on your provider and bank, this can take anywhere from two to five business days.

What is the difference between low-risk and high-risk merchant services?

Below are the high-level differences between the low-risk and high-risk merchant services:

| Category | Low-risk merchant services | High-risk merchant services |

|---|---|---|

| Typical industries | Restaurants, cafés, retail, automotive, and other stable or established industries. | Adult entertainment, weapons, online gambling, medical, CBD, and other high-risk sectors. |

| Approval & onboarding | Fast approval with minimal requirements. | Harder to get approved, with stricter underwriting requirements. |

| Processing costs | Lower fees per transaction. | Higher fees than standard market rates. |

| Contract terms | Short contracts with flexible terms and conditions. | Longer contracts with stricter rules and conditions. |

| Cash flow practices | Minimal rolling reserves or frozen funds. | Frequent rolling reserves and frozen funds to reduce risks. |

| Flexibility | Few restrictions on products/services or transaction volume. | Strict rules on what you can sell and how payments are processed. |

| Risk factors considered | Stable revenue, low chargeback ratio, and established business history. | New businesses, low credit score, delayed delivery, high chargeback ratio, non-standardized products, high processing volume, or dependency on time/materials. |

1. Low-risk merchant services

A low-risk merchant is a business that banks and merchant service providers see as having a low chance of payment fraud, chargebacks, or financial issues. If you’re low-risk, providers usually offer easier approval and require little to no additional risk-management measures. Low-risk businesses are often in stable, everyday industries such as restaurants, cafés, retail, and automotive.

Low-risk merchant services mean simpler approval, smoother onboarding, and lower processing costs compared to high-risk services. Providers also don’t apply strict rolling reserves or freeze funds, since they know you’re less likely to face fraud or frequent chargebacks.

2. High-Risk merchant services

High-risk merchants are businesses that pose a greater risk of chargebacks, fraud, or financial instability for providers. Common examples include industries like adult entertainment, weapons, online gambling, medical products, and CBD.

The riskier the business, the higher the fees and the harder it is to get approved. But industry type isn’t the only factor. Providers also consider:

- If your business is new and still building a reputation

- The financial stability of your business, or whether the owner has a low credit score

- The time between payment and delivery of products or services

- Whether your industry has a high chargeback ratio

- The level of product or service standardization

- Your processing amount and volume

- Dependencies your business relies on, such as time or materials

This means even a business in a “normal” industry can still be classified as high-risk. Every provider has its own way of evaluating risk, and they don’t publish the exact criteria to prevent fraudsters from gaming the system and slipping through the checks.

There are merchant service providers that specialize in serving high-risk merchants. However, the downside of high-risk merchant services is:

- Higher processing rates: This means every transaction costs you more compared to low-risk merchant services.

- Longer contract terms: Providers lock merchants into longer terms to protect themselves from the potential volatility of your business model.

- Less flexibility than traditional processors: You may face stricter rules around how you accept payments, the types of products or services you can sell, and the volume of transactions you can process each month.

- Frozen funds: If your merchant service provider spots any unusual activity, they can temporarily freeze your funds to investigate.

- Reserves on merchant accounts: Some providers withhold a percentage of your sales (known as a rolling reserve) for a set period, such as 90 days, to minimize their loss if fraud and chargebacks happen.

How to sign up for merchant services

To sign up for a merchant service, you first need to qualify for a merchant account. In the past, this meant filling out endless paperwork and going through extensive checks by banks. Today, the entire application process can be completed online.

In general, you’ll provide information about your business to a merchant service provider so they can approve your account and set you up with payment processing. The information you need to prepare includes:

- Business details: type of business, address, year of registration, etc.

- Product/service details: industry type, product or service description

- Processing details: currencies accepted, estimated monthly sales volume

- Tax details

- Business owner details

Once everything is submitted, the provider’s underwriting team will review it. It may take 48 hours or a few days to get the result. You don’t have to perfectly meet every requirement. The providers are always very flexible. If any concern comes up, they might request more info from you.

Learn more about how to qualify for a merchant account here.

Set up a merchant service and save 25% on processing fees with Helcim

Setting up merchant services with Helcim is simple. The online sign-up takes as little as five minutes, with no paperwork required.

Once approved, Helcim helps you get started by setting up your merchant account and providing any hardware or software you need to accept payments.

Why choose Helcim for your merchant services?

- Lower processing costs: Save up to 25% on credit card processing fees compared to other merchant service providers.

- All-in-one solution: Use a single merchant account to accept both in-person and online payments.

- Built-in tools: Get free access to invoicing, POS, payment gateways, virtual terminal, and all the tools you need to run your business.

- Transparent pricing: No monthly fees, no contracts, and no hidden charges. You only pay for what you process.

If you’re switching from another service merchant provider, Helcim’s Merchant Buyout Program covers up to $500 of your termination or equipment lease fees. Our team will also walk you through every step of migrating your data.

Break up with bad rates.

Feeling stuck with your provider? We'll waive $500 of your processing fees when you switch to Helcim.

Start your merchant services with Helcim today and enjoy seamless, cost-effective payment processing.

FAQ

Who pays the merchant service fee?

There are many types of merchant service fees, but transaction processing fees are the most common. Merchants are the ones who pay these fees. Each time a customer pays with a credit or debit card, a percentage of that transaction is deducted before the funds reach the business bank account. With Helcim Fee Saver, you can pass this cost to customers as a surcharge.

How can you avoid merchant service fees?

The only way to completely avoid merchant service fees is to stop accepting card payments and only take cash, checks, or direct bank transfers. Since that isn’t realistic for most businesses, you can minimize fees by encouraging customers to use lower-cost payment methods like debit cards or ACH/EFT transfers. You can also choose a merchant service provider that offers interchange-plus pricing to keep credit card processing costs lower.

What is the average merchant service fee?

On average, merchant service fees for credit cards range between 2% and 3.5% of each transaction. Debit card transactions are usually cheaper, sometimes under 1%. Fees vary depending on the card type (rewards cards cost more), the payment method (online vs. in-person), and your industry’s risk level. Most small businesses should budget around 2%–3% of card sales for processing fees.

How do merchant service providers make money?

Merchant service providers earn money by taking a small cut of each transaction processed. Part of your fee goes to the card networks and issuing banks, while the provider keeps its markup for facilitating the payment. Providers may also charge monthly fees, hardware costs, or incidental fees like chargeback fees. Essentially, the more payments you process, the more revenue the provider makes, which is why they aim to keep your transactions flowing smoothly.

Related Articles

-

Cash vs. credit: Should cash only businesses accept credit cards?

Kaitie Weaver | November 29, 2024

-

Merchant account fees uncovered: How to save on credit card processing costs

Jared Slemp | September 30, 2024

-

Merchant account: how to qualify for it?

Robert Luong | August 22, 2024

-

Merchant accounts: Overview, benefits, and cost.

Robert Luong | August 14, 2024

-

Credit Card Processing Fees Ultimate Guide

Ryleigh Stangness | July 1, 2022

-

How credit card processing works: An ultimate guide

Danny Randell | March 3, 2021