-

Content

Digital payments power modern commerce. Whether you're running an e-commerce store, SaaS platform, or retail shop, you need a reliable way to accept payments from customers.

The rapid growth of digital commerce has significantly increased demand for secure online payment systems. According to the World Bank, the global shift toward digital financial services has accelerated the adoption of electronic payments for both businesses and consumers.

That’s where payment service providers (PSPs) come in.

A payment service provider enables businesses to accept electronic payments, including credit cards, debit cards, ACH/EFT bank transfers, and digital wallet payments, through a single platform that connects merchants to payment networks and financial institutions.

In this guide, we’ll explain:

- What payment service providers are

- What do payment service providers do?

- How Payment Service Providers Work

- Payment service provider vs payment gateway vs payment processor vs bank

- What are different types of payment service providers?

- What are the benefits of payment service providers

- What are the typical fees for using a payment service provider

What is a payment service provider (PSP)?

A payment service provider (PSP) is a third-party company that enables businesses to accept electronic payments from customers. PSPs act as intermediaries between merchants, customers, banks, and card networks, facilitating secure payment authorization and settlement. According to the Bank for International Settlements, payment service providers play a critical role in connecting merchants with the financial infrastructure required to process digital payments.

Instead of integrating with multiple financial institutions individually, businesses can use a PSP to access many payment methods through a single integration.

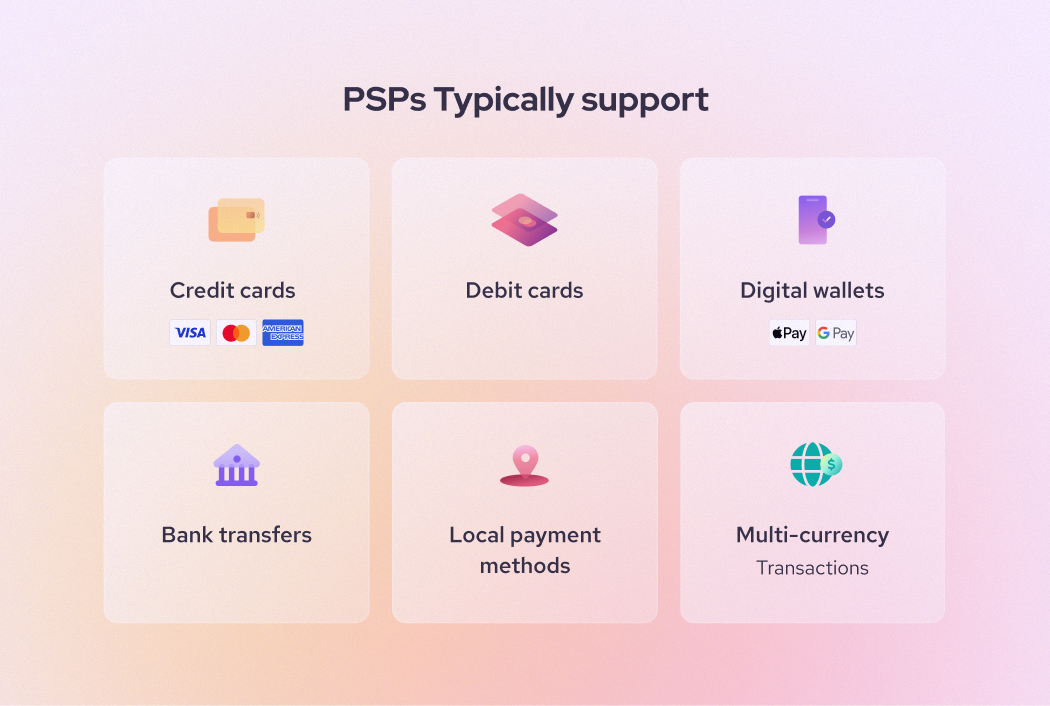

Which payment methods do payment service providers typically support:

- Credit cards (Visa, Mastercard, Amex)

- Debit cards

- Digital wallets (Apple Pay, Google Pay)

- Bank transfers

- Local payment methods

- Multi-currency transactions

Many payment service providers (PSPs) also combine merchant accounts, payment gateways, fraud tools, and reporting into a single platform. This integrated approach simplifies payment infrastructure for businesses and reduces the technical complexity required to accept digital payments.

This makes payment service providers especially popular with small businesses and online merchants that want to start accepting payments quickly.

What do payment service providers do?

Payment service providers (PSPs) handle the infrastructure that allows businesses to accept, process, and manage digital payments. Instead of merchants building payment systems themselves, PSPs provide a single platform that connects businesses to payment networks, issuing banks, and financial institutions.

Beyond simply processing payments, payment service providers also provide tools for security, reporting, and global payment acceptance.

The key functions of a payment service provider are:

- Processing payments

- Offering payment gateway technology

- Supporting multiple payment methods

- Providing fraud prevention and security technology

1. Payment Processing

At the core of any payment service provider is payment processing.

Payment service providers (PSPs) facilitate the transfer of funds between customers and merchants by communicating with multiple financial institutions involved in a transaction. A typical payment transaction involves several entities including payment processors, card networks, issuing banks, and acquiring banks working together to authorize and settle payments. Learn more about how credit card processing works.

When a customer submits payment details, the payment service providers:

- Encrypts the payment information

- Sends the transaction request to the payment processor

- Routes the request through the card network (Visa, Mastercard, etc.)

- Receives authorization from the issuing bank

- Confirms the transaction to the merchant

This entire process typically occurs within seconds, allowing customers to complete purchases instantly. According to the Federal Reserve, modern payment processing infrastructure enables real-time authorization for most card transactions while settlement occurs later between financial institutions.

Payment service providers handle millions of these transactions daily and maintain the infrastructure necessary to ensure high reliability and low transaction latency.

2. Payment Gateway Technology

Many payment service providers include a payment gateway as part of their platform.

A payment gateway is the secure technology that captures payment information from a checkout page or POS system and sends it to the payment processor for authorization.

For example, when a customer enters their credit card details on an ecommerce website:

- The gateway encrypts the card data

- Sends it to the payment processor

- Receives approval or rejection

- Returns the result to the checkout page

Gateways ensure that sensitive payment data is transmitted securely using encryption protocols such as SSL and tokenization.

These security measures are aligned with standards defined by the Payment Card Industry Data Security Standard (PCI DSS), which establishes requirements for protecting cardholder data during payment transactions.

Some payment service providers provide hosted checkout pages, while others provide online payment integration like APIs that allow developers to build custom payment experiences directly into their websites or mobile apps.

3. Multi-Payment Method Support

Modern consumers expect flexibility when paying for goods and services. Payment service providers enable businesses to accept multiple payment methods through a single integration.

Depending on the provider, merchants may accept:

- Credit cards

- Debit cards

- Digital wallets (Apple Pay, Google Pay)

- Buy Now Pay Later services

- Bank transfers

- Local payment methods

This is particularly important for international ecommerce, where payment preferences vary significantly across regions. Research from the Bank for International Settlements shows that local payment methods often dominate domestic payment markets even as global card networks expand internationally.

For example:

- Interac is widely used in Canada

- iDEAL is common in the Netherlands

- Alipay dominates in China

By supporting multiple payment methods, payment service providers help merchants increase checkout conversion rates and reduce cart abandonment by allowing customers to pay using familiar and trusted payment options.

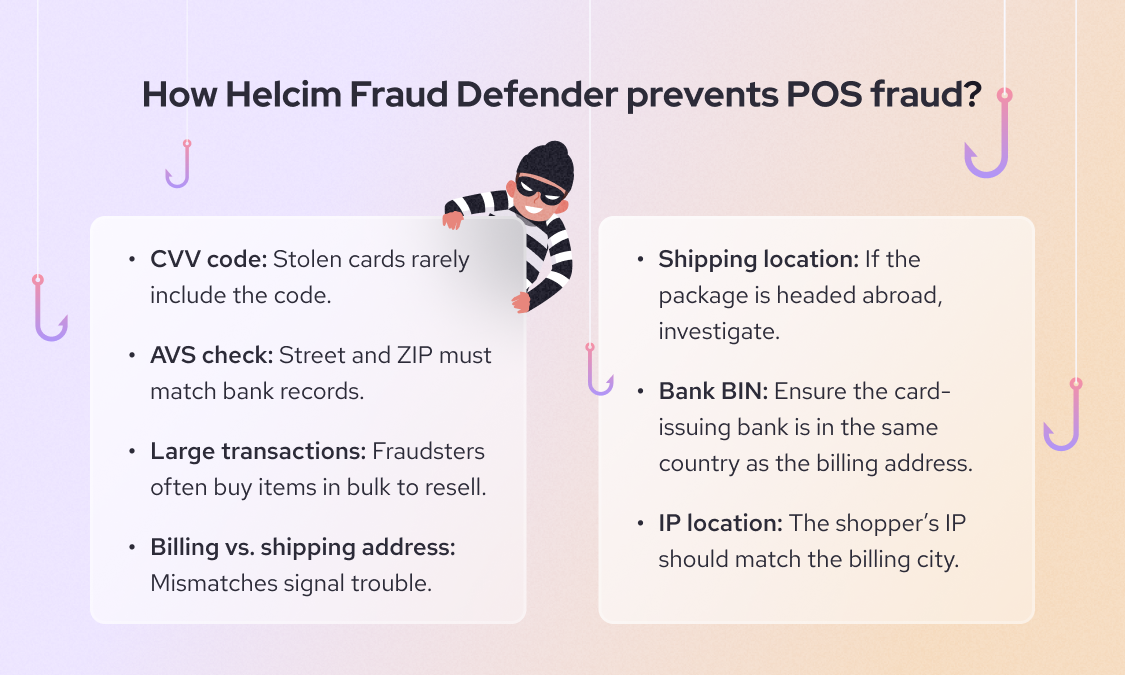

4. Fraud Prevention and Security

Payment security is one of the most critical responsibilities of a payment service provider. Payment service providers implement advanced security technologies to protect both merchants and customers from fraud and data breaches.

Common security measures include:

- PCI DSS compliance to meet industry security standards

- Tokenization, which replaces card data with secure tokens

- Encryption of payment information during transmission

- 3D Secure authentication for cardholder verification

- AI-based fraud detection systems

These tools monitor transactions in real time to detect suspicious activity such as unusual purchase patterns or high-risk locations.

The PCI Security Standards Council, which manages the PCI DSS framework, requires payment systems to follow strict guidelines for storing, processing, and transmitting cardholder data.

By handling these security responsibilities, payment service providers help merchants reduce fraud risk and maintain compliance with financial regulations.

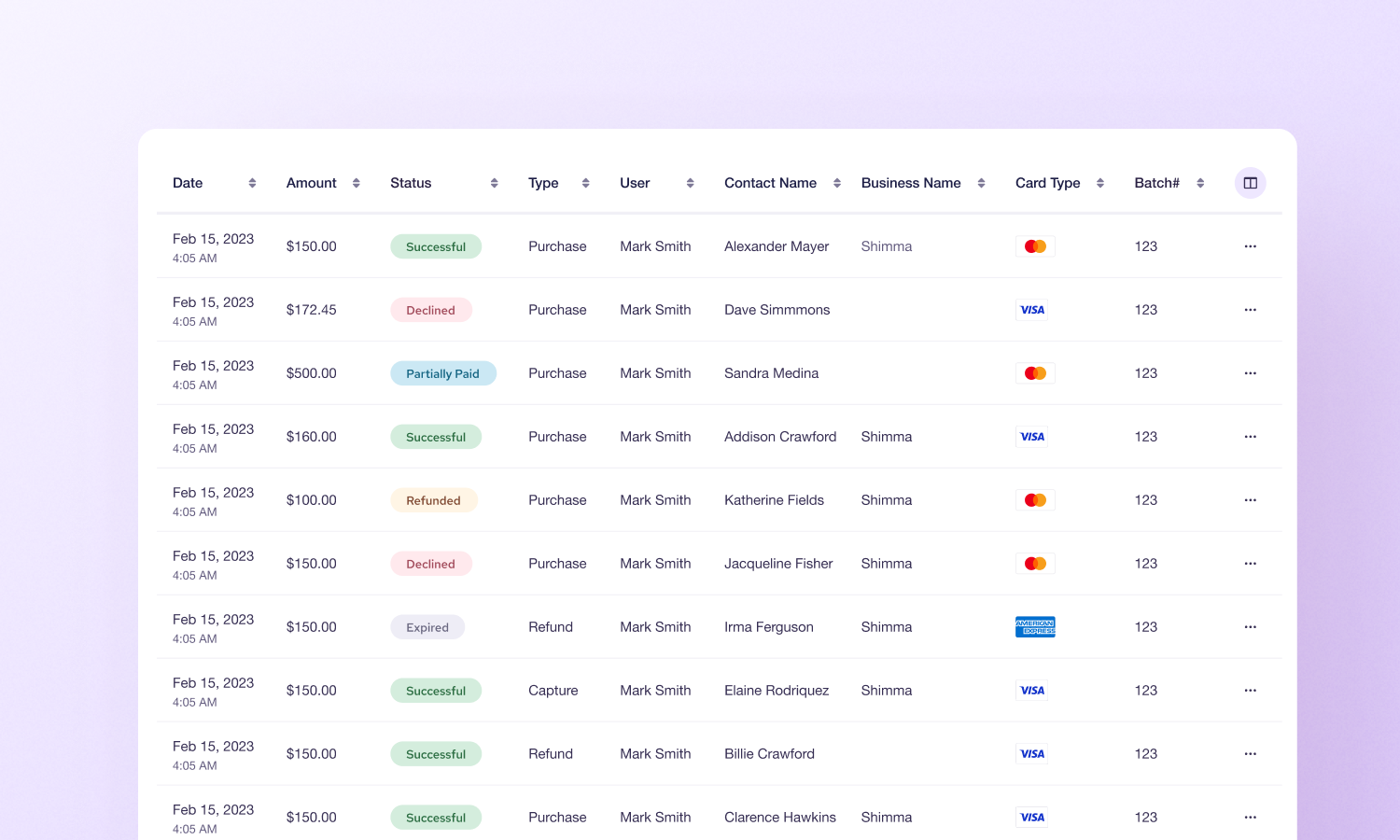

5. Reporting and Analytics

Most payment service providers provide dashboards that allow businesses to monitor their payment activity in real time.

These analytics tools typically include:

- Transaction history

- Payment success and decline rates

- Revenue reporting

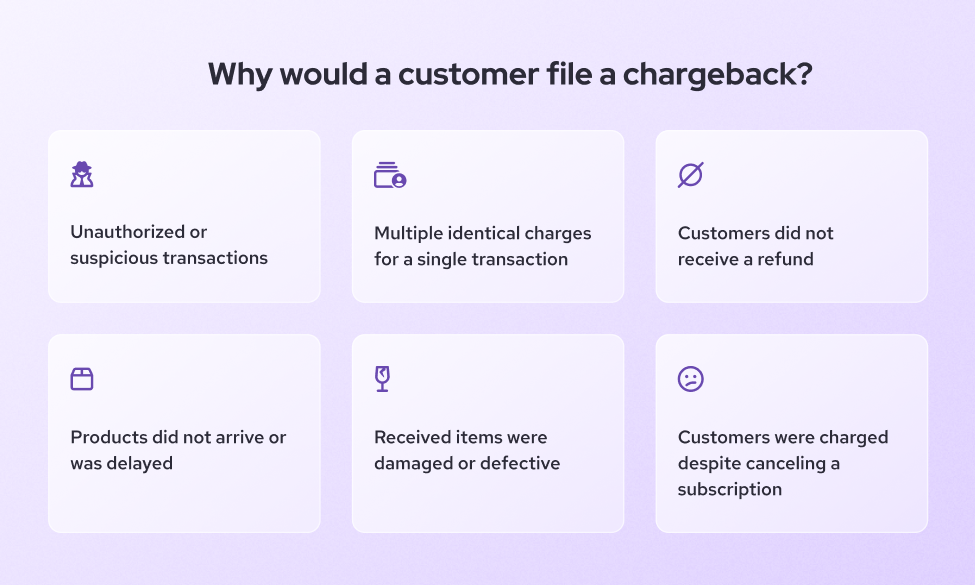

- Chargeback tracking

- Refund management

Merchants can use these payment data to better understand customer behavior, identify payment failures, and optimize their checkout experience.

For example, analytics may reveal that a large percentage of customers abandon checkout due to declined cards or unsupported payment methods.

With this information, businesses can improve payment acceptance rates and increase revenue.

6. Global Payment Infrastructure

Many payment service providers allow businesses to accept payments international customers.

Global payment service providers support:

- Multiple currencies

- Cross-border transactions

- Local payment methods

- International settlement

This infrastructure makes it easier for businesses to expand into new markets without building local banking relationships.

For example, an ecommerce business in Canada can sell products to customers in Europe or Asia while allowing those customers to pay using their preferred local payment methods.

Payment service providers handle currency conversion, payment routing, and settlement so merchants can operate internationally with minimal complexity.

How do payment service providers work?

A payment service provider manages the entire payment transaction lifecycle, from the moment a customer submits their payment details to the final settlement of funds in the merchant account.

Behind a simple checkout experience is a complex network of financial institutions, payment processors, card networks, and security systems working together to authorize and settle transactions securely.

Payment service providers simplify this process by acting as the central technology layer that connects merchants to the broader payments ecosystem.

Below is a simplified overview of how a typical payment transaction works when using a payment service provider:

- Customer initiates payment: A customer enters payment details on a website, credit card machine, or mobile payment app.

- Payment data is encrypted: The payment service provider encrypts the payment information to ensure security.

- Authorization request is sent: The payment service provider sends the payment request to the card network and issuing bank.

- Bank approves or declines: The issuing bank checks funds and fraud signals before approving or rejecting the transaction.

- Merchant receives confirmation: The merchant receives approval and the payment is captured.

- Funds settle to a merchant account: The payment service provider transfers the funds to the merchant’s account after settlement. This process usually happens in seconds, although settlement may take 1–3 business days. Learn more about payment processing time here.

Payment service provider vs payment gateway vs payment processor vs bank

These terms are often used interchangeably, but they refer to different parts of the payment stack.

| Component | What it Does |

|---|---|

| Payment Service Provider |

|

| Payment Gateway |

|

| Payment Processor |

|

| Acquiring Bank |

|

A payment service provider often bundles all of these functions into one platform, which simplifies setup for businesses.

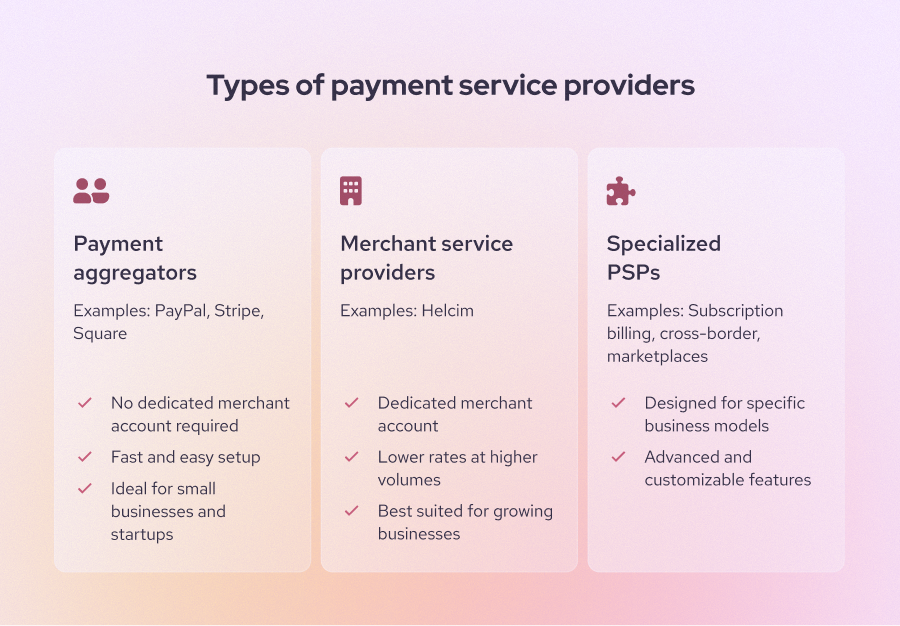

What are different types of payment service providers?

There are several types of payment service providers (PSPs) depending on their payment model.

- Payment aggregators

- Merchant service providers

- Specialized payment service providers

1. Payment Aggregators

Payment aggregators allow merchants to accept payments without creating their own merchant account. Instead, they use a single master merchant account to process transactions for thousands of small businesses. Because the aggregator handles the "heavy lifting" with the banks, merchants can simply sign up, get approved, and start accepting payments almost instantly.

However, because payment aggregators onboard many merchants quickly, they monitor account activity very closely. For example, if you suddenly process an unexpectedly high volume of credit card transactions, your funds may be held or frozen for review. In some cases, it can take weeks or even months to resolve these holds and receive your money.

Examples include:

They process payments under a master merchant account, allowing businesses to start accepting payments quickly.

2. Merchant Service Providers

These providers offer dedicated merchant accounts with customized pricing and underwriting. This model involves a more rigorous upfront review to verify that your business is legitimate. While you will need to provide more financial documentation during the application process, once you are approved, it means your business is established and faces a much lower risk of account interruptions or fund freezes.

Benefits include:

- Lower transaction fees for high volume

- Greater control over payments

- More advanced integrations

3. Specialized Payment Service Providers

These providers not only move money, but they also solve specific business problems. Some providers focus on specific payment types:

Examples:

- Subscription billing platforms

- Cross-border payment providers

- Marketplace payment infrastructure

- Digital wallet integrations

What are the benefits of payment service providers

Using a PSP offers several advantages for businesses.

- Faster setup: Businesses can start accepting payments without negotiating directly with banks. Because the entire process is handled online, you can set up your account, import customers, configure taxes, and test transactions to start accepting payments right away.

- Multiple payment methods: Modern payment service providers like Helcim let you accept credit cards, debit cards, and ACH payments. Customers can pay using their preferred payment options.

- Simplified compliance: All payment service providers must be PCI Level 1 compliant. The PSPs manage PCI DSS security requirements and provide fraud detection. This allows you to accept payments securely and prevent hackers from stealing your customer or business information.

- Global reach: Many payment service providers support multi-currency payments and international customers. As a result, businesses can collect payments from clients around the world. However, keep in mind that international transactions typically cost more than domestic ones.

- Better customer experience: Payment service providers provide various features that streamline the checkout process. Faster checkout and payment flexibility can increase conversion rates. For example, Helcim offers a Tap to Pay on iPhone option, allowing US-based businesses to accept contactless payments anywhere directly on their phones.

What are the typical fees for using a payment service provider?

The typical fees for using a payment service provider are transaction fees (from 2.3% to 3.5%), monthly platform fees ($10 - $100 or more), chargeback fees ($15 - $30), international payment processing fees (an additional 1% to 2% on top of transaction fees).

1. Transaction fees

This is the primary source of income for payment service providers. It is usually a percentage plus a fixed amount. For example, 2.9% + $0.30 per transaction.

There are two types of pricing model that payment service providers are offering:

- Flat-Rate Pricing: It’s a fixed fee of 2.9% + $0.30

- Interchange-Plus Pricing: The most transparent model. The payment service providers pass exactly what banks and payment networks charge you (it fluctuates every transaction), plus a transparent markup on top. For example,, Interchange + 0.20% + $0.10. This is often much cheaper for high-volume businesses.

2. Monthly platform fees

Some payment service providers charge monthly subscription fees, from $10 to $100 per month. Businesses often subscribe to these plans to access business management features, advanced reporting or specialized tools for their industries.

3. Chargeback fees

The credit card chargeback fees are charged when customers dispute a transaction. These fees can range from $15 to $30 per chargeback. Helcim refunds this fee back to you if you provide the evidence and successfully dispute the chargeback.

4. Cross-border fees

Businesses need to pay additional fees for international payments.

- Cross-Border Fees: An additional 1% to 2% added to transactions where the customer’s card was issued in a different country.

- Currency Conversion (FX) Fees: A markup (typically 1% to 3%) applied when you accept a foreign currency and want it to be converted into your currency in your bank account.

Are using payment service providers safe?

Security is essential for payment processing. Payment service providers protect transactions using:

- PCI DSS compliance: The payment service providers help your business accept, process, store, or transmit credit card information securely, reducing the risk of data theft.

- Tokenization: Payment service providers ensure that even if your business's database is breached, the hackers only find useless tokens rather than actual credit card numbers.

- Encryption: Payment service providers make it impossible for cybercriminals to read sensitive payment information while it travels across the internet.

- Fraud monitoring: Payment service providers detect and notify you when there are fraudulent transactions so that you can review the transaction and make a final decision. This helps protect both the merchant and the consumer. Learn how to prevent in-person payment frauds and online payment frauds.

These safeguards help protect sensitive payment data from breaches and fraud.

Final Thoughts

Payment service providers have become essential infrastructure for modern businesses.

By simplifying payment processing, supporting multiple payment methods, and ensuring secure transactions, PSPs enable businesses to focus on growth rather than payment technology.

Choosing the right provider depends on your:

- transaction volume

- payment methods

- geographic markets

- pricing requirements

With the right PSP, businesses can deliver faster checkout experiences, expand globally, and increase revenue.

Frequently Asked Questions

What is an example of a payment service provider?

Examples include Stripe, PayPal, Adyen, Square, and Helcim.

Is a bank a payment service provider?

Not usually. Banks provide financial accounts, while payment service providers provide payment infrastructure that connects businesses to card networks and banks.

How long is payment service provider processing time?

Most payment service providers settle funds within 1–3 business days, although settlement speed varies depending on the payment method.

Do I need a merchant account to use a payment service provider?

When you sign up with a payment service provider like Stripe, Square, or Helcim, you have a credential to log in to your account. This account is a part of the master merchant account that payment service providers have with the bank.

What payment methods do a payment service provider support?

Most modern payment service providers support all major credit and debit cards like Visa, Mastercard, American Express, and Discover. They also typically integrate popular digital wallets such as Apple Pay, Google Pay. Beyond cards, many providers offer support for ACH/EFT bank transfers.

Related Articles

-

What Do Payment Processors Do?

Alivia Massimillo | April 16, 2024

-

How can I accept online ACH payments?

Ryleigh Stangness | August 29, 2023

-

Credit Card Processing Fees Ultimate Guide

Ryleigh Stangness | July 1, 2022

-

.gif)

How to Accept Credit Card Payments Online and In-person

Humayun Farooq | October 17, 2020