Alright, you're running a business, you're making sales, and then comes the tap, the swipe, the digital wallet magic – the credit card payment. It's a must-have in today's world. But if you're like a lot of small business owners, you've probably glanced at your processing statement and thought, "Hmm, interesting... So how exactly does this whole credit card processing thing work on the other side? How do these processors actually get their cut?" It's a question that's probably crossed your mind, and honestly, it's a smart one to ask. So without further ado, let's pull back the curtain and take a look at how credit card processors get paid.

The building blocks: Credit card processing fees broken down

Before we get into how the processors get paid, it's important to understand what makes up the cost of processing a credit card payment in the first place. There are a few key players and their associated fees that all come together and take a small piece of the payments pie. Let's break down the different costs involved in each swipe, tap, or click.

1. Interchange fees: The card network's cut

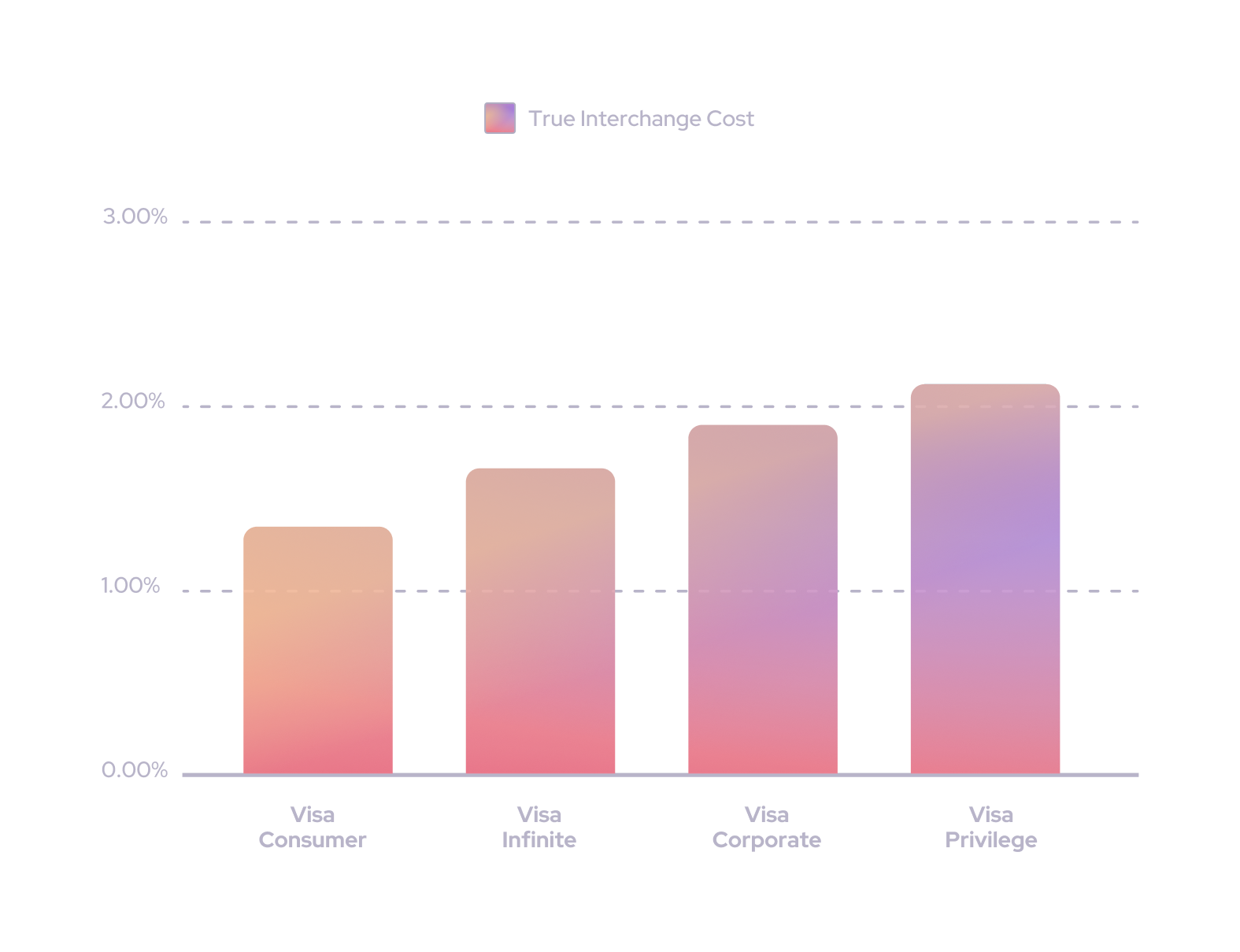

Think of Visa, Mastercard, Discover, and American Express as the rule-makers of the credit card world. They set the guidelines and facilitate the transactions. Interchange fees are paid by your business's bank (the acquiring bank) to the customer's bank (the issuing bank) for each credit card transaction.

What it is: A per-transaction fee charged by the card networks (like Visa and Mastercard) and paid to the bank that issued the customer's credit card.

Why it matters: Interchange fees make up the largest portion of your processing costs and are non negotiable. The exact amount varies widely depending on factors like the type of card used (premium rewards cards usually have higher interchange), the merchant category code (MCC) of your business, and how the transaction was processed (in-person vs. online).

2. Assessment fees: Paying the card network for the privilege

On top of interchange, the card networks also charge assessment fees. Think of this as a fee for using their brand and network infrastructure.

What it is: A smaller percentage-based fee paid directly to the card network (Visa, Mastercard, Discover, Amex).

Why it matters: While typically smaller than interchange, assessment fees are unavoidable and are usually a percentage of the total transaction volume. These fees help the card networks cover their operating costs and invest in their systems.

3. Processor markup: How the payment processor makes money

This is where the company that provides your credit card processing services gets paid. The markup is the fee they add on top of the interchange and assessment fees.

What it is: The fee charged by your payment processor for their services. This can be structured in various ways, such as a percentage of the transaction, a fixed per-transaction fee, or a combination of both.

Why it matters: The processor's markup covers their costs for providing the technology, customer support, security features, and other services that enable you to accept credit card payments. This is the area where pricing can vary most between different processors.

By understanding these core components – interchange, assessment fees, and the processor's markup – you start to get a clearer picture of where the costs of accepting credit cards come from. Now that we know the ingredients, let's look at how the processors put it all together to get paid.

How much does a credit card processor make?

We know that processors add a markup to the underlying interchange and assessment fees. But the way they apply this markup and the other fees they charge can vary. Here are some common ways payment processors generate revenue:

- Margin on each transaction. Each pricing model gives different profits to the payment processors

- Extra fees on premium payment tools and features

- Monthly subscription fees for merchant services

- Hardware leasing fees

- Other hidden fees

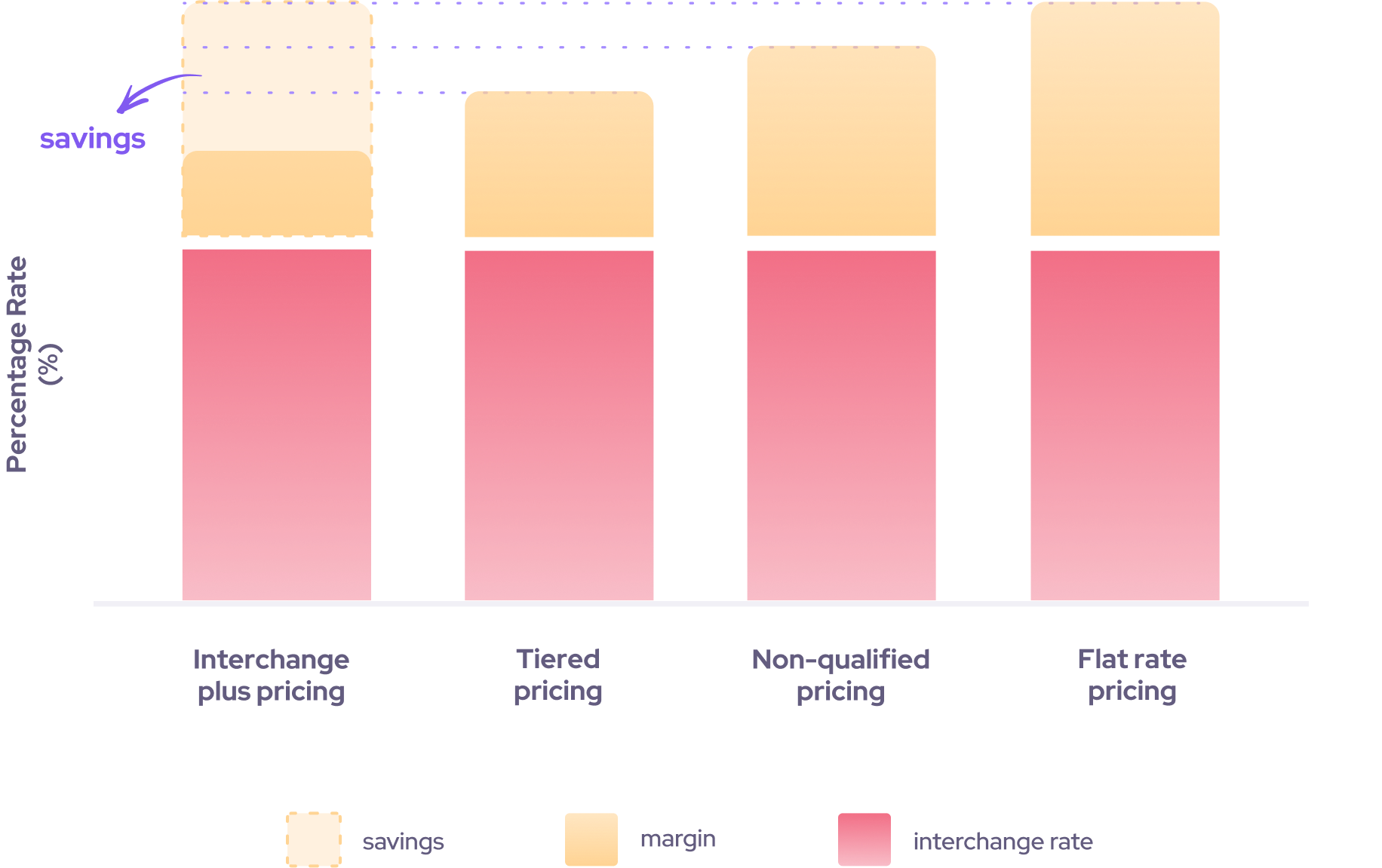

1. Margin on transactions: The processor's cut

This is the most direct way processors make money – by adding a margin on top of the costs they incur (interchange and assessment). This margin can be structured in a few different ways:

Flat-rate pricing: Simplicity at a cost

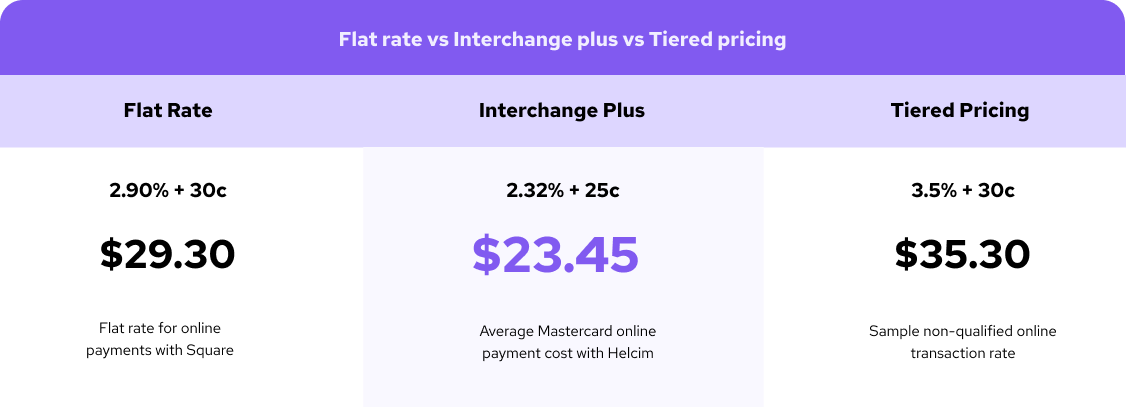

- What it is: A straightforward pricing model where you pay a single, fixed percentage plus a small per-transaction fee for every credit card transaction, regardless of the card type. For example, you might see a rate like 2.9% + $0.30 per transaction.

- How the processor makes money: The processor sets this flat rate higher than the average interchange and assessment fees they pay. The difference between the flat rate and their underlying costs becomes their profit margin.

- Example: If a transaction has an underlying cost (interchange + assessment) of 1.8% + $0.10, and the processor charges you 2.9% + $0.30, their margin on this transaction is 1.1% + $0.20.

- Good for: Businesses with low transaction volume and smaller average ticket sizes who value predictability. However, it can be more expensive for businesses with higher volume transactions.

Interchange-plus pricing: Transparency and potential savings

- What it is: A more transparent model where the processor charges you the direct interchange and assessment fees (the "interchange-plus" part) plus a separate, clearly stated markup. This markup can be a percentage, a fixed per-transaction fee, or a combination of both (e.g., interchange + 0.2% + $0.10).

- How the processor makes money: The processor earns their revenue directly from the added markup. Because the interchange and assessment fees are passed through at cost, their profit is solely determined by their stated markup.

- Example: If a transaction has an interchange fee of 1.5% and an assessment fee of 0.1%, the total underlying cost is 1.6%. If the processor's markup is 0.3% + $0.05, your total processing fee would be 1.9% + $0.05. The processor's profit on this transaction is the 0.3% + $0.05.

- Good for: Businesses of all sizes, especially those with higher transaction volumes, as it can often lead to lower overall costs compared to flat-rate pricing, especially for transactions with lower interchange rates.

2. Access costs: Premium tools and payment features

Many processors offer additional tools and features beyond basic payment processing, and they often charge extra for these.

- What it is: Fees for accessing advanced features such as analytics dashboards, fraud protection tools, advanced reporting, customer relationship management (CRM) integrations, or specialized payment gateways.

- How the processor makes money: By offering these valuable add-ons, processors create additional revenue streams from businesses that need these functionalities. The pricing for these tools can be a one-time fee, a recurring subscription, or tiered based on usage or features.

- Hot tip: Not all processors charge extra for premium tools or features to scale your business. Helcim, for example, allows merchants to access one free account with no monthly fees. All the tools are included with no additional charges. You only pay for what you process.

3. Monthly subscription fees: A recurring revenue stream

Some processors charge a flat monthly fee for using their platform and services, regardless of the transaction volume.

- What it is: A fixed fee charged on a monthly basis for access to the processor's platform, customer support, and basic processing capabilities.

- How the processor makes money: This provides a predictable and recurring revenue stream for the processor. The monthly fee might be bundled with a specific transaction pricing model.

- Good for: We don't believe an unnecessary fee is good for any business. Seasonal businesses or businesses with very low transaction volume might find this fee even more frustrating than most.

4. Hardware lease fees: Revenue from equipment

If your business requires physical payment terminals, some processors offer the option to lease the equipment instead of purchasing it outright.

- What it is: A recurring fee (usually monthly) for the use of payment processing hardware, such as countertop terminals, mobile card readers, or point-of-sale (POS) systems.

- How the processor makes money: Leasing hardware provides a steady stream of income for the processor over the term of the lease. While it can lower the upfront cost for businesses, the total cost of leasing over time can sometimes exceed the cost of purchasing the equipment.

5. Other potential fees: Additional revenue sources

Beyond the main categories, processors might also charge other fees for specific services or events, such as:

- Statement fees: A fee for generating and sending your monthly processing statement (though many now offer digital statements for free).

- Chargeback fees: Fees charged when a customer disputes a transaction, to cover the costs of investigating and resolving the dispute.

- ACH processing fees: Fees for processing electronic check (ACH) payments.

- Setup fees: A one-time fee to establish your processing account (be wary of high setup fees).

- Early termination fees: Fees charged if you cancel your processing agreement before the end of the contract term.

- Non-compliance fees: Fees for not adhering to PCI DSS security standards.

By understanding these various ways payment processors generate revenue, you can better evaluate different pricing models and choose a processor that aligns with your business needs and offers a fair and transparent cost structure.

How to avoid overpaying your credit card processor

Nobody wants to feel like they're throwing money away, especially when it comes to essential business services like credit card processing. The good news is, there are definitely smart ways to approach this and ensure you're getting a fair deal. Here's what to look out for:

1. Demand transparent pricing

The first step in not overpaying is understanding exactly what you're being charged. This means looking beyond simple flat rates and digging into the details. Ask potential processors about their pricing models. Are they offering interchange-plus pricing? This model gives you a clear view of the underlying costs (interchange and assessments) and the processor's margin. Transparency here is key.

2. Be wary of bundled costs and hidden fees

Some processors might lure you in with a seemingly low rate, but then hit you with a barrage of extra hidden payment charges. Keep an eye out for monthly subscription fees just for having an account, premiums to access essential tools or reporting features, statement fees, or excessive fees for things like chargebacks. A truly transparent processor will be upfront about all potential costs.

3. Understand your volume and transaction types

The best pricing model for your business depends on how much you process and the types of cards your customers use. Businesses with lower volumes might find flat-rate pricing simpler to budget for, but as you grow, interchange-plus pricing can often lead to significant savings, especially on transactions with lower interchange rates.

4. Don't get locked into long-term contracts

Long-term contracts can sometimes come with early termination fees that make it difficult to switch to a better provider if you find one. Opt for processors that offer more flexible agreements.

5. Evaluate the "free" extras

Sometimes, processors offer "free" hardware or software, but these costs might be recouped through higher processing rates or other hidden fees down the line. It's crucial to look at the total cost of ownership, not just the initial offer.

6. Shop around and compare

Just like you'd compare prices for any other essential business service, take the time to get quotes from multiple credit card processors. Compare their pricing structures, fees, and the value of the services they offer.

Save on credit card fees with Helcim

At Helcim, we believe in keeping things straightforward and fair. That's why we've built our pricing around the transparent interchange-plus model. You pay the direct costs of interchange and assessments, plus a clear markup based on your monthly processing volume.

We also don't believe in nickel-and-diming our merchants. You won't find monthly platform fees just to have an account, or extra charges to access our suite of powerful tools and reporting. The price you see is the price you pay for processing – nothing hidden, no surprises. You simply pay for the transactions you process.

See your potential savings with Helcim

Want to get a clearer picture of how much you could save with a transparent pricing model? We offer a free credit card rate calculator on our website. It allows you to input your current processing information and see a potential comparison. It's a simple way to understand the impact of transparent pricing on your bottom line.

By being informed and asking the right questions, you can navigate the world of credit card processing and find a partner that offers fair and transparent pricing, helping you keep more of your hard-earned revenue where it belongs – in your business.

FAQs

How are payment processing fees generally determined by credit card processors?

Different companies charge for credit card processing in different ways. The processing fees you pay to accept payments could depend on several factors, such as:

- The pricing model and your processor's margin

- The interchange rate

- The card and transaction type

- Your business industry

How is the interchange rate determined?

Processing fees are broken up into two portions: The interchange fee and the processor’s margin.

Interchange Rates for card brands like Visa and Mastercard are determined by the card brands and issuing banks. All credit card processors adhere to the exact same interchange rates. To arrive at this base cost for each transaction, they take into consideration factors such as:

- Type of payment card

- Card brand

- The type of business accepting the card

- The transaction type

- The cost of processing this transaction

- Risk factors such as fraud

- Consumer rewards and perks

The second portion of your processing costs - the processor margin - is made up by your payment processor. How much you pay to accept payments will depend on which pricing model your processor uses and how much they make from their margin.

Does Helcim charge equipment leasing fees?

No, Helcim does not lease our equipment and we try to warn merchants against leasing equipment from other providers. Instead, we offer affordable equipment and accessory options which you can purchase outright from us, avoiding costly leases and contracts. Unlike other providers, Helcim has no contracts or cancellation fees.

How does Helcim handle chargebacks in its pricing model?

Helcim offers a competitive rate of $15 per chargeback transaction, but we waive the fee altogether if the merchant wins their dispute.

How do Helcim's rates compare to Square's?

Helcim uses an Interchange Plus pricing model, whereas Square charges users a flat rate. Our pricing models afford merchants transparent pricing with no hidden fees while passing on the savings of lower interchange rates instead of charging a flat rate and a large margin. Learn more in our Helcim vs. Square article. Law firms and other businesses that require separate trust and operating bank accounts are able to customize the flow of deposits and fees to meet their needs.